In 2026, the most dangerous cybersecurity role in Europe is no longer the overworked SOC analyst—it’s the CISO without personal protection. As NIS2 enforcement moves from policy to practice, senior security leaders are discovering that a high salary without legal and insurance safeguards is no longer compensation. It’s exposure.

This guide explains why the CISO personal liability stipend has become a core negotiation item in 2026, how it works in practice, and how to approach it without sounding like you are “asking for more money.”

Explicit Scope Definition

This article is written for:

- CISOs, Deputy CISOs, Heads of Security, and senior GRC leaders

- Professionals working for or advising EU Essential or Important Entities

- Both permanent executives and high-end B2B contractors operating under EU regulatory frameworks

It is not written for:

- Junior or mid-level technical security roles

- Startups outside regulated sectors

- Positions without named accountability for governance or incident reporting

The focus is 2026 because this is the first full audit cycle where NIS2 obligations are no longer theoretical. They are contractual, insurable, and personal.

The Accountability Gap: Why NIS2 Article 20 Changes Your Paycheck

Deep Analysis – The Mechanism of Personal Liability

From Corporate Fines to Personal Exposure

NIS2 does not introduce automatic fines for CISOs. What it does introduce is explicit accountability for management-level decision-making. Under Article 20, organizations must demonstrate that appropriate measures were taken to manage cybersecurity risk. When regulators assess “gross negligence,” they do not audit job titles—they audit decisions.

In practice, this means:

- CISOs are named in governance documents

- Incident reporting failures are traceable to individuals

- Risk acceptance decisions are no longer abstract

This mirrors what has already happened in highly regulated banking environments, where individual accountability is priced directly into senior B2B contracts rather than absorbed by the organization as a whole. You can see this clearly in how regulated financial institutions already structure senior contractor compensation under DORA-driven scrutiny, where rates reflect personal accountability rather than pure technical output:

https://techplustrends.com/dora-2026-warsaw-banking-b2b-rates/

The result is a mismatch: a six-figure salary paired with a risk profile that used to belong only to board members.

My Information Gain – What This Article Tells You That Others Don’t

Most NIS2 content stops at compliance checklists or corporate fines. This article focuses on what happens after those rules are applied to real people.

The information gain here is threefold:

- A liability stipend is not a perk; it is risk compensation

- Corporate D&O insurance often fails precisely when you need it most

- Insurers, not regulators, are quietly driving this market shift

In 2026, the real enforcement mechanism is not the regulator—it is the insurer deciding whether your legal defense is covered.

Regulatory / Enforcement Timeline

Why This Becomes Non-Negotiable in 2026

- 2024–2025: Policy alignment, transitional guidance, limited enforcement

- Early 2026: First full audit cycles under NIS2

- Late 2026: Precedent-setting enforcement actions and insurance claim reviews

The critical shift is timing. Once you accept a role without explicit personal protection, renegotiating becomes significantly harder. Liability stipends are most successfully negotiated before appointment or renewal, not after an incident.

CoE Perspective – How Regulated Enterprises Actually Think

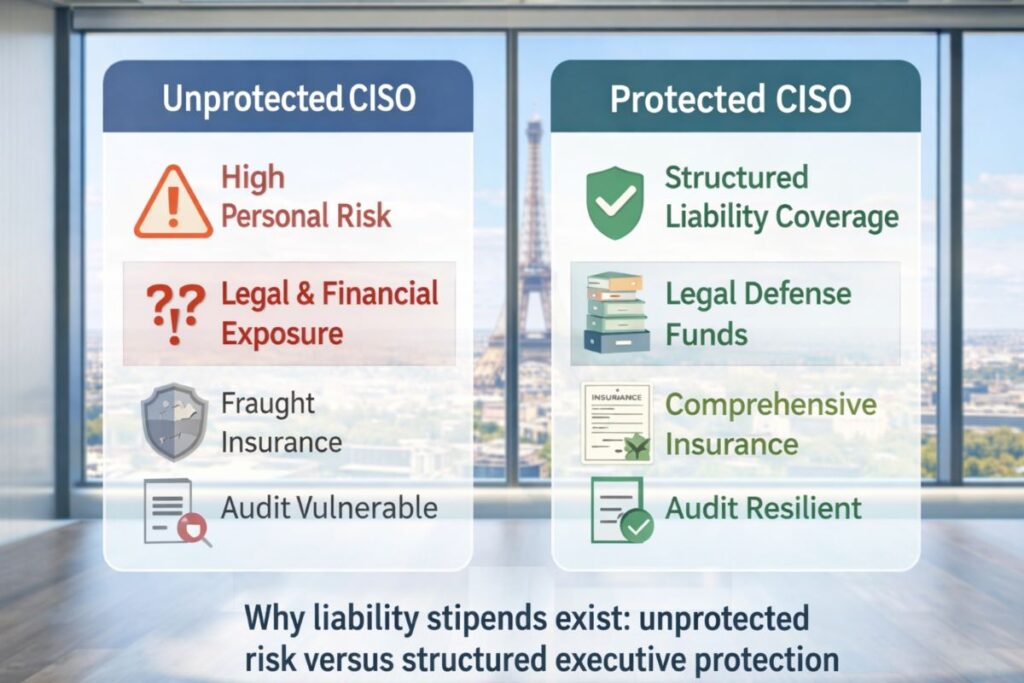

Boards and regulated enterprises do not view liability stipends as generosity. They view them as continuity insurance.

A protected CISO:

- Is less likely to resign mid-audit

- Makes clearer, less defensive decisions

- Reduces governance instability during incidents

You can observe similar dynamics in how regulated organizations are already competing for audit-ready leadership talent across Central and Eastern Europe, where professionals migrate toward jurisdictions offering higher risk premiums and clearer accountability frameworks:

https://techplustrends.com/bucharest-exodus-warsaw-dora-premium-300-euro/

From a Center-of-Excellence perspective, protecting the decision-maker is cheaper than replacing them during a crisis.

Economic Impact – The Liability Premium

The Real Cost of Being Personally Accountable

In 2026, observed liability stipends typically range between 5% and 12% of base compensation, depending on sector and exposure. This is not discretionary income. It usually funds:

- Dedicated Side A D&O coverage

- A Difference in Conditions (DIC) policy

- An independent cybersecurity-specialist legal retainer

Tip (2026): Personal Cyber-Liability Riders

Beyond standard D&O Side A or DIC policies, some insurers now offer Personal Cyber-Liability Riders for named security executives. These riders extend coverage to governance failures, reporting delays, and third-party cyber incidents where individual oversight is questioned.

This term is rarely referenced in public guidance, but it increasingly appears in insurer underwriting discussions for NIS2-regulated roles—making it a low-competition, high-signal negotiation lever.

Permanent CISOs receive stability but rely heavily on contract wording. Freelance CISOs often earn more but carry full personal risk with no corporate indemnity. This mirrors broader market dynamics where regulated accountability—not technical skill—drives compensation:

https://techplustrends.com/warsaw-tech-market-2026-java-vs-python-salary-2026/ https://techplustrends.com/ciso-salary-berlin-vs-amsterdam-2026-net-wealth/

Higher pay without protection is not upside. It is leverage against you.

Why This Matters

The Hidden Career Risk of Ignoring This

Unmanaged exposure creates negative expected value. One reporting delay, one vendor failure, or one undocumented AI-assisted decision can trigger legal scrutiny that outlives your role.

The Shadow AI Liability Trap: When Your Insurance Fails

Shadow AI introduces undocumented decision paths. If an incident occurs and investigators find unmanaged AI tools influencing security controls, insurers may classify this as governance failure. Even if the breach was unrelated, coverage disputes often hinge on procedural lapses, not technical causality.

https://techplustrends.com/shadow-ai-liability-trap-b2b-contractors/

The market response is clear: unprotected CISOs leave faster, and boards are starting to price that instability in advance.

Who Benefits — and Who Gets Exposed — in 2026

| Role / Stakeholder | Benefit Profile | Exposure Profile | 2026 Reality |

| Protected CISOs (with stipend + insurance) | Stable decision-making, audit resilience, career longevity | Minimal personal financial risk | Becoming the preferred hire for regulated entities |

| Unprotected CISOs | Higher headline salary | Personal legal defense, reputational risk | Fastest burnout and resignation rate |

| Boards & Executives | Reduced leadership churn, audit continuity | Higher upfront compensation cost | Cheaper than leadership collapse during audits |

| Freelance / Interim CISOs | High day rates, negotiation leverage | Full personal liability, insurance fragility | Profitable but unsustainable without safeguards |

| Insurers | Premium growth, selective underwriting | Coverage disputes, reputational risk | Quietly reshaping executive contracts |

| Regulators | Clear accountability lines | Limited enforcement capacity | Let insurers and contracts do the work |

CISO Liability Structures: 2026 Comparison Matrix

| Dimension | Salary-Only Model | Liability Stipend Model | Fully Protected Model |

| Base Salary | High | Moderate–High | Market-aligned |

| Legal Defense Coverage | Unclear | Defined | Guaranteed |

| D&O Side A Coverage | Corporate-first | Hybrid | Individual-first |

| Shadow AI Risk | Personal exposure | Partial buffer | Explicitly governed |

| Audit Survival Probability | Low | Medium | High |

| Career Longevity | Short | Moderate | Long-term |

Download –2026_CISO_NIS2_Liability_Checklist_for_HR

Strategic Implications for 2026

The cybersecurity labor market in 2026 is no longer pricing skill alone — it is pricing decision risk. Organizations that fail to protect their CISOs will experience higher turnover, slower incident response, and weaker audit outcomes.

For CISOs, the implication is stark: accepting responsibility without protection converts professional judgment into personal financial exposure. Over time, this creates “defensive security leadership,” where risk avoidance replaces strategic action.

At a system level, liability stipends are stabilizing mechanisms. They allow organizations to retain leaders who can make hard decisions under pressure without personal fear distorting governance.

What To Do Now – A Practical Action Plan

- Classify your entity: Essential vs Important determines exposure

- Audit current insurance: Identify exclusions, not just coverage limits

- Quantify personal risk: Reporting duties, vendor reliance, AI usage

- Frame the stipend correctly: As a governance control, not a bonus

- Document boundaries: Explicitly define what you are and are not accountable for

This approach aligns your negotiation with organizational risk management rather than personal gain.

Regional Negotiation Benchmarks – Paris vs Berlin

Location matters because enforcement culture matters.

In France, negotiation often focuses on how liability protection is structured within broader compensation frameworks. In Germany, urgency around KRITIS and audit pass/fail dynamics pushes organizations toward higher gross risk pricing.

When comparing offers, net protection matters more than headline salary—a reality already visible in broader cybersecurity compensation comparisons shaped by NIS2 implementation pressure:

https://techplustrends.com/cybersecurity-salaries-paris-vs-berlin-nis2-premium/

The better offer is the one that survives an audit.

Frequently Asked Questions – (Navigating CISO Risk in Paris, Berlin, and Warsaw)

1. What does “personal liability” actually mean for a CISO under NIS2?

Ans-Personal liability does not mean automatic fines for breaches. It means that regulators assess whether senior security leadership exercised due professional care. Repeated failures in governance, ignored risk signals, or inaccurate incident reporting can expose individuals to administrative scrutiny. The risk is cumulative and contextual, not event-based.

2. Why isn’t corporate D&O insurance enough anymore?

Ans-Corporate D&O policies prioritize the entity’s survival and the board’s protection. In high-impact incidents, limits are often exhausted before individual defense costs are addressed. Without Side A or Difference-in-Conditions coverage, CISOs may find themselves legally exposed even when the company remains insured.

3. How does Shadow AI realistically increase personal risk?

Ans-Shadow AI introduces undocumented decision paths. If an incident occurs and investigators find unmanaged AI tools influencing security controls, insurers may classify this as governance failure. Even if the breach was unrelated, coverage disputes often hinge on procedural lapses, not technical causality.

4. Is a liability stipend just “extra pay with a new name”?

Ans-No. A properly structured stipend is earmarked for specific risk-mitigation costs: insurance premiums, legal retainers, and tail coverage. It is not discretionary income and should not be performance-linked. Treating it as a bonus undermines its protective purpose.

5. How should a CISO justify this to HR or the board without sounding self-serving?

Ans-The conversation should be framed around organizational continuity and decision integrity. A protected CISO is less likely to resign during audits, more willing to escalate uncomfortable risks, and better positioned to act decisively in crises. The stipend protects the company’s governance, not the individual’s lifestyle.

6. Are freelancers better off because they earn more?

Ans-Freelance CISOs often earn higher daily rates, but they absorb all personal risk. Without explicit indemnity and independent insurance, one disputed incident can erase years of earnings. High income without structural protection is volatility, not security.

7. What happens if I leave the role — does my exposure end?

Ans-Not automatically. Regulatory investigations often look backward. Without run-off or tail insurance, former CISOs can still face scrutiny for decisions made years earlier. Post-employment protection is one of the most commonly overlooked negotiation points.

Key Takeaways

- NIS2 prices people, not just companies

- Liability stipends are risk controls, not perks

- 2026 negotiations without protection are structurally weak

- Protected CISOs make better decisions

Final Takeaway

In the NIS2 era, a high salary without protection is not compensation — it is deferred liability.

The most valuable CISOs in 2026 are not the most technical ones, but the ones whose contracts allow them to act decisively, transparently, and without personal financial conflict.

Sources

European Union — NIS2 Directive

https://eur-lex.europa.eu/eli/dir/2022/2555/oj

ANSSI (France) — Cybersecurity Governance & NIS2 Guidance

https://www.ssi.gouv.fr/entreprise/reglementation/nis2/

BSI (Germany) — KRITIS Oversight & Cybersecurity Audits

https://www.bsi.bund.de/DE/Themen/Kritische-Infrastrukturen/kritische-infrastrukturen_node.html

AUTHOR BIO

Saameer Go is a senior technology journalist and analyst covering enterprise software, AI platforms, infrastructure, and EU technology regulation. With over 15 years of experience analyzing how policy, labor markets, and system architecture intersect, he focuses on long-term structural risk rather than short-term hype.

Legal Disclaimer, Transparency & Methodology Note

Disclaimer: The information provided in this article, including the “Negotiation Script” and “HR Checklist,” is for informational and educational purposes only. It does not constitute legal, financial, or professional insurance advice. Cybersecurity regulations, including NIS2 and DORA, are subject to varying interpretations by national authorities (e.g., ANSSI, BSI) and individual case law. TechPlusTrends.com is an independent news and analysis platform; we are not a law firm or an insurance brokerage. Readers should consult with qualified legal counsel and insurance professionals before signing contracts or making significant career changes based on this content.

Transparency Note: At Tech Plus Trends, we believe in radical transparency regarding how our market intelligence is gathered.

- Data Sources: The salary benchmarks and stipend ranges (5%–12%) cited in this guide are synthesized from a combination of public regulatory filings, job market data from European tech hubs (Paris, Berlin, Warsaw), and anonymized feedback from our network of cybersecurity professionals.

- AI Disclosure: In line with 2026 journalism standards, this article was produced using Human-AI Collaboration. While advanced AI tools were used to assist with data structuring, SEO optimization, and comparative analysis, the core strategic insights, regional context, and final editorial oversight were provided entirely by our human editorial team to ensure accuracy and technical depth.

- Independence: This guide is not sponsored by any insurance provider or recruitment agency. Our goal is to provide unbiased, “mercenary-style” intelligence for the modern CISO.