AI data centers in 2026 produce waste heat at 55°C–65°C from liquid-cooled GPU racks — hot enough to sell directly into municipal heating networks at €25–45/MWh. This guide covers the thermal architecture, EED compliance, Heat Purchase Agreements, city-by-city deployment landscape, and the real economics of district heating integration for European AI campuses.

Key Takeaway

District heating AI data centers are becoming a core component of European AI infrastructure in 2026 — not as a sustainability gesture, but as a financially material infrastructure decision. Liquid-cooled Blackwell GPU racks operating at 120–150 kW produce coolant exit temperatures of 55°C–65°C, which is directly injectable into 4th Generation District Heating (4GDH) networks without industrial heat pumps. For a 100 MW AI campus near a municipal heating network, this translates to €25–35 million in annual heat sales revenue, a measurable PUE improvement, and compliance with EU Energy Efficiency Directive Article 26(6) waste heat recovery mandates. The operators who treat this as optional will face both a revenue gap and a permit problem.

What District Heating AI Data Centers Are — And Why 2026 Is the Inflection Point

A district heating AI data center is a liquid-cooled high-density computing facility that exports its thermal output to a municipal heating network, allowing waste heat from GPU clusters to warm residential buildings, offices, and industrial processes.

The concept is not new. What changed in 2026 is the thermal physics.

Traditional enterprise data centers running air-cooled servers at 5–15 kW per rack produced waste heat at 25°C–35°C. That temperature is too low for direct municipal heating use — 4GDH networks require supply temperatures of 45°C–65°C. Bridging that gap required industrial heat pumps with Coefficients of Performance (COP) of 3–5, adding capital cost and operational complexity that made the economics marginal in all but the most favorable locations.

NVIDIA Blackwell deployments operating at 120–150 kW per rack changed the equation structurally. Direct liquid cooling systems remove heat at the GPU die, and the coolant exits at 55°C–65°C — within the direct-injection range of most 4GDH networks without any heat boosting. The heat pump requirement is eliminated. The economics become compelling. And Article 26(6) of the recast EU Energy Efficiency Directive makes the assessment of waste heat reuse legally mandatory for facilities above 1 MW.

This convergence — higher rack temperatures, native 4GDH compatibility, and regulatory obligation — is why district heating integration has moved from sustainability pilot to standard design consideration for any new European AI campus above 1 MW in 2026.

Understanding the power profile that produces this thermal output is essential context. For a full breakdown of how AI workload power requirements drive thermal output at different rack densities, see our complete AI data center power requirements guide.

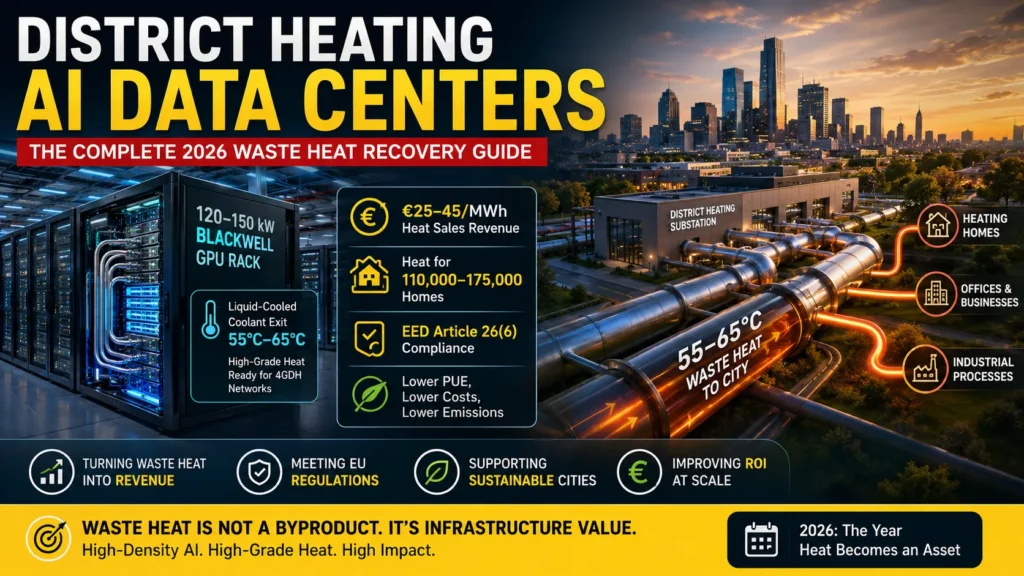

How Much Waste Heat Does an AI Data Center Actually Produce?

This is the question most infrastructure guides avoid because the answer requires showing the arithmetic. Here it is.

The physics: Every watt of electrical power consumed by a computing system eventually becomes heat. A GPU that consumes 1,000W produces approximately 1,000W of thermal output. At facility scale, total thermal output equals total electrical input minus a small amount of work done by the compute (which is negligible for heat recovery calculations).

At 100 MW facility scale:

- Electrical input: 100 MW

- Thermal output: ~97–99 MW (at PUE 1.03–1.05 with DLC)

- Coolant exit temperature (Blackwell DLC): 55°C–65°C

- Recoverable heat (accounting for thermal losses in heat exchange): ~75–85 MW

- Annual thermal energy available for export: ~660,000–745,000 MWh

What those heats: A modern European apartment building requires approximately 50–80 kWh/m² annually for space heating. A typical apartment of 80m² requires 4,000–6,400 kWh/year. At 700,000 MWh of annual exported heat, a 100 MW AI campus can supply the heating needs of approximately 110,000–175,000 apartments — comparable to a significant portion of a mid-sized European city’s residential heating demand.

These numbers are why municipalities in Stockholm, Copenhagen, Helsinki, and Amsterdam are actively competing to site AI campuses near their district heating networks rather than treating data center heat as a nuisance to be managed.

For context on how this thermal output scales at gigawatt level, see our 1GW data center power and infrastructure guide.

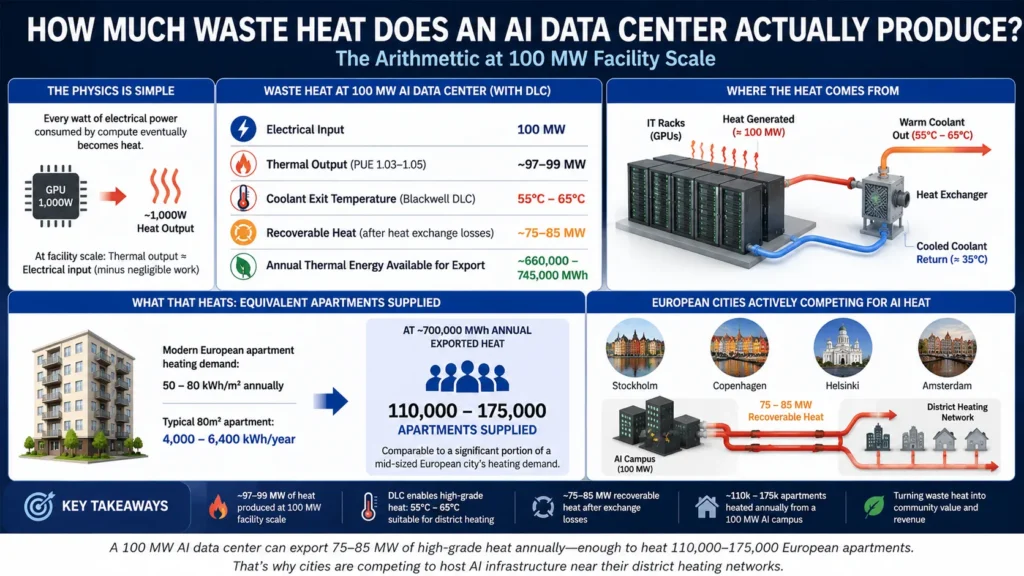

The Thermal Architecture: How Heat Moves from GPU to City

The engineering of waste heat recovery in an AI data center involves three thermally isolated loops, each with distinct operating parameters and failure modes.

Loop 1 — Primary: Direct Liquid Cooling at the Rack

Cold plates are mounted directly on GPU die packages. Coolant — typically water with corrosion inhibitors, or a dielectric fluid — enters the cold plate at approximately 28°C–32°C and exits at 55°C–65°C after absorbing heat from the GPU.

This exit temperature is the breakthrough that makes 4GDH integration viable. Previous-generation air-cooled and rear-door heat exchanger systems could not achieve this temperature lift, which is why heat recovery from legacy data centers required industrial heat pumps to boost temperatures to district-usable levels.

Key design parameters for Loop 1:

- Flow rate: sized for GPU thermal design power (TDP) plus safety margin

- Pressure rating: 4–6 bar for most DLC systems

- Fluid chemistry: monitored continuously for pH, conductivity, and biological contamination

- Variable-speed pump control: essential for AI workloads, which are thermally bursty

For a detailed treatment of how Blackwell hardware’s thermal requirements are reshaping European facility design from the rack up, see our guide to Blackwell infrastructure deployments across Europe.

Loop 2 — Secondary: Building Thermal Transfer

A plate heat exchanger (PHE) isolates the primary data hall cooling loop from the building export loop. This isolation is non-negotiable — it prevents any contamination of the municipal heating supply from data center coolant chemistry, and it protects rack-level cooling systems from pressure fluctuations in the building loop.

The PHE transfers approximately 90–95% of the thermal energy from Loop 1 to Loop 2, with a 2°C–5°C temperature drop across the exchanger. The building export loop operates at slightly lower temperature (50°C–60°C) and higher flow volume than the primary loop.

Variable-speed pumps in Loop 2 must respond to AI workload variability. GPU utilization can shift by 40–60% within seconds during inference burst cycles. Thermal management systems need predictive controls — typically AI-based — that anticipate workload changes rather than reacting to them, to prevent thermal oscillations that reduce heat exchanger efficiency.

Loop 3 — Tertiary: Municipal Network Connection

The thermal substation connects the building export loop to the municipal district heating network. This is where the data center becomes a city energy supplier.

In standard 4GDH configurations, heat is injected into the network return pipe at 45°C–55°C, preheating municipal water before it reaches central boilers. This reduces the boiler load and fuel consumption of the municipal heating system.

In advanced deployments where coolant exits at 65°C+, direct supply-pipe injection is possible — the data center becomes a distributed heat source within the municipal network rather than a return-pipe preheater. This configuration commands higher prices under Heat Purchase Agreements but requires more precise temperature control.

The HVDC connection: Operators combining HVDC power distribution with district heating integration achieve efficiency compounding — lower electrical conversion losses mean more power reaches compute, and liquid cooling captures heat at higher temperatures from more efficiently powered GPUs. This integrated approach is covered in our HVDC data centers Europe power guide.

The Economics: Heat Purchase Agreements and the Revenue Model

The business model for district heating integration has matured from informal arrangements to structured long-term contracts that resemble utility power purchase agreements.

Heat Purchase Agreement (HPA) Structure

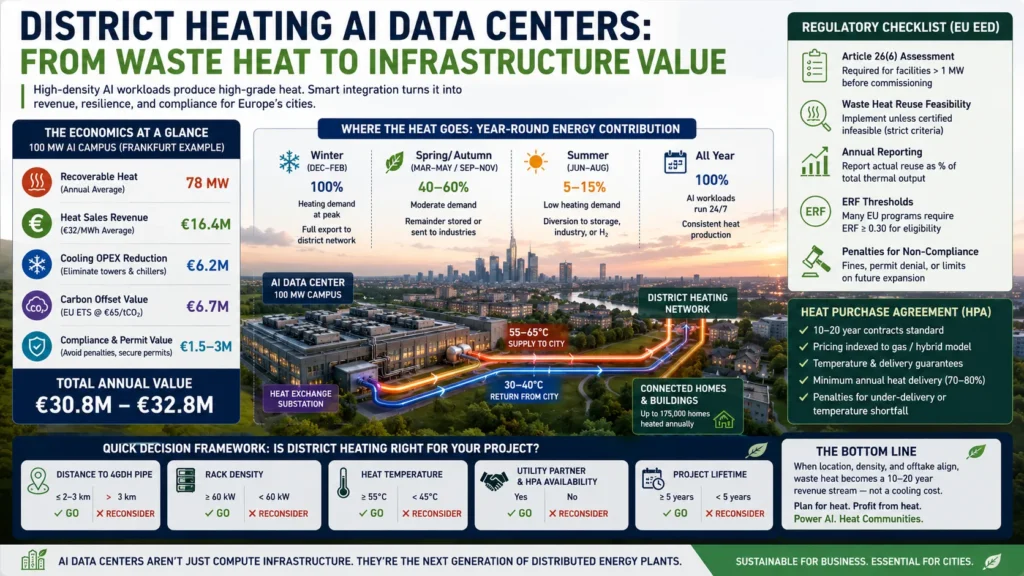

A Heat Purchase Agreement is a long-term contract between a data center operator and a district heating utility specifying:

- Thermal floor and ceiling commitments — the operator guarantees minimum annual heat delivery (typically 70–80% of theoretical capacity) and the utility pays for actual delivered heat up to a contracted maximum

- Pricing structure — typically indexed to local gas prices or a hybrid of gas index plus fixed component, reviewed annually

- Temperature specifications — minimum supply temperature contractually required; penalties apply if average monthly temperature falls below threshold

- Duration — 10–20-year terms are standard in Nordic markets; shorter 5–7-year terms common in newer markets

- Grid priority provisions — some contracts allow utilities to reduce offtake during low-demand periods (summer), with data centers compensated for available but unused capacity

Current HPA pricing ranges:

- Nordic markets (Stockholm, Helsinki, Copenhagen): €35–45/MWh — highest in Europe due to mature 4GDH networks and high alternative fuel costs

- German markets (Frankfurt, Munich, Berlin): €28–38/MWh

- Dutch markets (Amsterdam, Rotterdam): €25–35/MWh

- UK markets (London, Manchester): £28–40/MWh

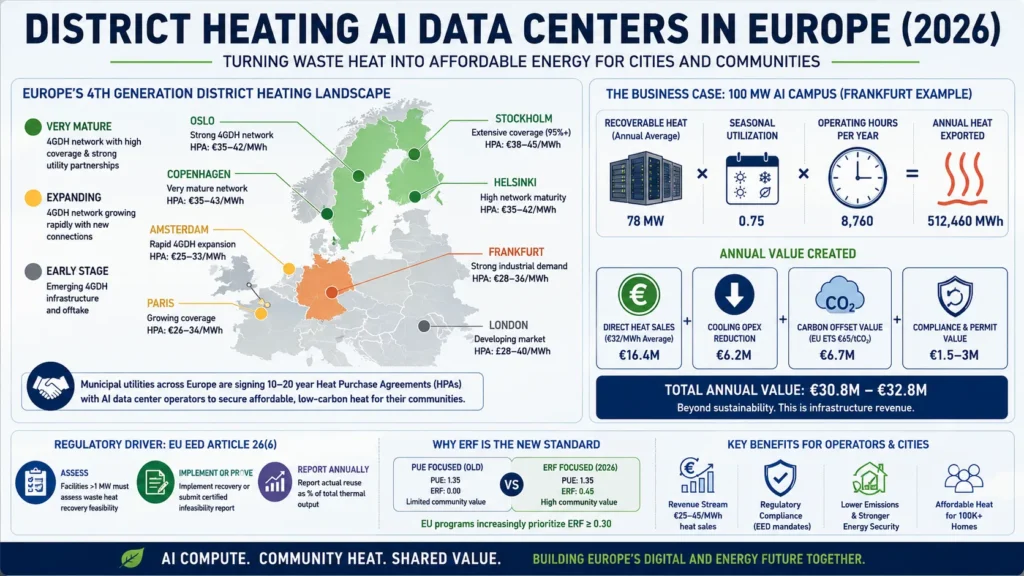

Revenue Stack: Worked Example for a 100 MW AI Campus

Assumptions:

- Facility: 100 MW electrical input, Blackwell DLC, Frankfurt location

- Recoverable heat: 78 MW average (accounting for summer reduction)

- Operating hours: 8,760/year

- Average HPA price: €32/MWh (Frankfurt mid-range)

- Cooling OPEX baseline (without heat recovery): €12M/year

- Carbon credit value: EU ETS at €65/tonne CO₂

Revenue calculation:

- Annual heat exported: 78 MW × 8,760 hours × 0.75 seasonal utilization = 512,460 MWh

- Direct heat sales: 512,460 MWh × €32/MWh = €16.4M

- Cooling OPEX reduction (eliminated cooling towers, reduced chiller load): €6.2M

- Carbon offset value (replacing gas heating): 512,460 MWh × 0.20 tCO₂/MWh × €65 = €6.7M

- Permit and regulatory compliance value (avoids EED non-compliance penalties): €1.5–3M depending on facility scale

Total annual value: €30.8–32.8M

This derivation is why the €25–35M figure appears in infrastructure planning models — it is not an estimate but a calculation from actual HPA pricing, realistic seasonal utilization, and current EU carbon pricing.

For operators evaluating the full AI infrastructure cost stack including power procurement, the AI data center power requirements guide for 2026 provides the electrical cost baseline against which heat recovery ROI should be calculated.

EU Regulatory Framework: Article 26(6) and the ERF Mandate

The regulatory dimension of district heating integration is not optional for European operators in 2026. Understanding exactly what is required — and what the penalties for non-compliance look like — is essential for any facility planning above 1 MW.

Article 26(6): The Waste Heat Assessment Mandate

Under the recast EU Energy Efficiency Directive (EED), facilities with total IT power above 1 MW must:

- Conduct and submit a waste heat recovery feasibility assessment to national authorities before commissioning

- Implement waste heat reuse measures unless a certified infeasibility assessment demonstrates technical or economic barriers

- Report annually on actual waste heat recovered and reused as a percentage of total thermal output

The infeasibility exemption is narrower than most operators assume. If a 4GDH network pipe exists within 2 km of the facility boundary, regulators in Germany, Netherlands, and Denmark have consistently rejected infeasibility claims on cost grounds. The pipe extension cost (typically €1.5M–€3M per km) is treated as a cost of doing business, not a barrier to feasibility.

Practical implication: Any new facility above 1 MW siting within 2 km of a 4GDH network in Germany, Netherlands, France, or the Nordic markets should treat district heating integration as a planning baseline, not an optional upgrade.

ERF: The Metric That Now Matters More Than PUE

Power Usage Effectiveness (PUE) remains the headline efficiency metric in industry benchmarking. The EU regulatory framework has introduced a second metric — Energy Reuse Factor (ERF) — that is increasingly determinative for facility permits and sovereign compute program eligibility.

ERF formula: ERF = Energy exported and reused externally ÷ Total energy input to IT equipment

ERF examples:

- A facility with 100 MW IT load exporting 60 MW of heat to a district network: ERF = 0.60

- A facility with 100 MW IT load and no heat recovery: ERF = 0.00

- Target ERF for EU sovereign compute program eligibility: ≥ 0.30 in most national frameworks

Why ERF can outweigh PUE for permitting: A facility with PUE 1.35 but ERF 0.45 exports significantly more energy value to the surrounding community than a facility with PUE 1.08 but ERF 0.00. Under current EU policy frameworks, the higher-ERF facility may receive more favorable treatment for expansion permits — even though its internal efficiency is lower.

This regulatory logic reflects the EU’s broader objective: data centers should contribute to the energy system, not just consume from it.

This ERF-first framework is directly embedded in the sovereign AI infrastructure programs across France, Germany, and Nordic markets. For a full analysis of how energy metrics interact with sovereign compute program requirements, see our EU sovereign AI infrastructure stack guide.

City-by-City Deployment Landscape: Where District Heating Integration Works Best

4GDH network maturity, local heating demand, regulatory enforcement, and utility partnership appetite vary significantly across European markets. Here is the current landscape for the six most relevant markets.

| City/Market | 4GDH Coverage | HPA Price Range | Regulatory Pressure | Integration Timeline | Key Utility Partner |

| Stockholm | Very high (95%+ city coverage) | €38–45/MWh | High | 12–18 months | Fortum Värme |

| Copenhagen | Very high | €35–43/MWh | Very high | 10–16 months | HOFOR, Vestforbrænding |

| Helsinki | High | €35–42/MWh | High | 12–20 months | Helen Ltd |

| Frankfurt | High (expanding) | €28–36/MWh | Strict | 18–30 months | Mainova |

| Amsterdam | Moderate (expanding) | €25–33/MWh | Strict | 20–36 months | Vattenfall Warmte |

| Paris | Moderate | €26–34/MWh | High (sovereign programs) | 18–28 months | CPCU |

Stockholm is the most mature market. Fortum Värme has been contracting waste heat from data center operators since 2017, and the city’s 4GDH network covers virtually the entire municipality. Integration timelines are the shortest in Europe because the utility processes have been standardized through repeated deployments.

Copenhagen is following a similar trajectory, with aggressive municipal targets to source 100% of district heating from waste heat and renewables by 2030. Data centers near the city are being actively recruited as heat sources.

Frankfurt presents the largest volume opportunity due to Germany’s size and the density of hyperscale deployments in the Rhine-Main corridor. The regulatory environment is strict, and the Article 26(6) feasibility assessment process is well-established through Mainova’s partnership program.

Amsterdam is undergoing rapid 4GDH expansion specifically in response to data center concentration. Vattenfall Warmte has extended pipes to the Amsterdam Science Park and ArenA Boulevard zones specifically to create offtake capacity for data center waste heat.

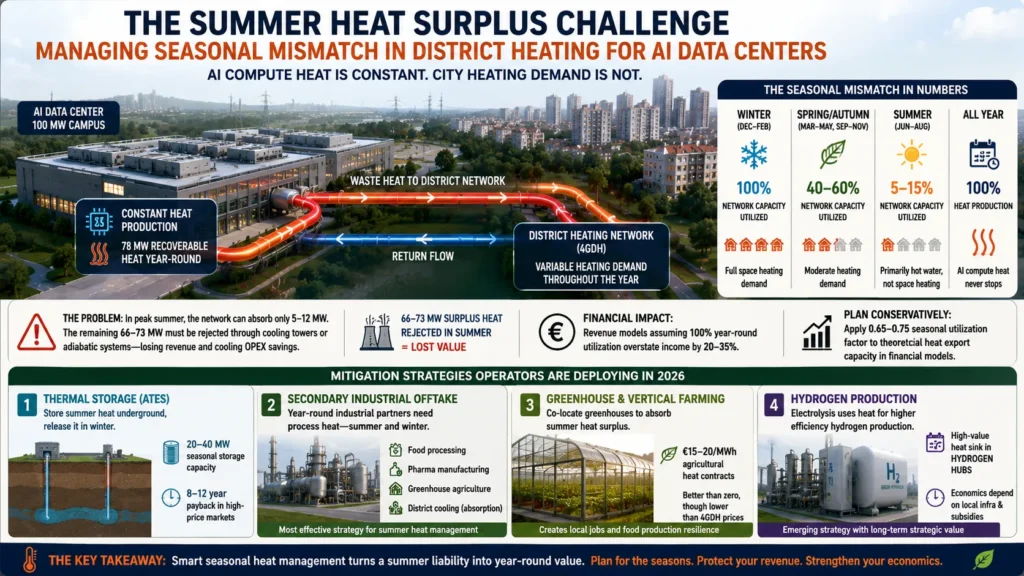

Seasonal Demand Management: The Summer Heat Surplus Problem

One of the most under addressed challenges in district heating integration is the mismatch between AI compute heat production (year-round, relatively constant) and residential heating demand (strongly winter-weighted, near-zero in summer).

The problem in numbers:

- Winter heating demand: 100% of 4GDH network capacity utilized

- Spring/autumn heating demand: 40–60% of network capacity utilized

- Summer heating demand: 5–15% of network capacity (primarily hot water, not space heating)

A 100 MW AI campus exporting 78 MW of recoverable heat year-round faces a situation where the district network can absorb most of its output in winter but only 5–12 MW in peak summer. The remaining 66–73 MW must be rejected elsewhere — typically through cooling towers or adiabatic systems — which eliminates the revenue and the cooling OPEX savings for those months.

Mitigation strategies operators are deploying in 2026:

Thermal storage: Underground aquifer thermal energy storage (ATES) systems can absorb summer heat and release it in winter. Large-scale ATES installations capable of 20–40 MW seasonal storage are becoming cost-effective at AI campus scale, with 8–12-year payback periods in high-price markets.

Secondary industrial offtake: The most effective summer heat management strategy is establishing secondary offtake contracts with industrial heat users — food processing, pharmaceutical manufacturing, greenhouse agriculture, and district cooling absorption chillers — that need process heat year-round regardless of season.

Greenhouse and vertical farming integration: Several European operators have co-located greenhouse facilities adjacent to AI campuses specifically to absorb summer heat surplus. At €15–20/MWh for agricultural heat contracts, the economics are weaker than 4GDH sales but substantially better than zero.

Hydrogen production: Electrolysis for green hydrogen production is emerging as a high-value summer heat sink in markets near industrial hydrogen demand. The economics depend heavily on local hydrogen infrastructure and subsidy frameworks.

Practical planning implication: Revenue models that assume year-round HPA utilization are overstating annual income by 20–35%. Conservative models should apply a 0.65–0.75 seasonal utilization factor to theoretical annual heat export capacity.

Who Is Doing This Now: Named Operators and Deployments

The district heating market for AI data centers is no longer a pilot program. Named deployments are operating at commercial scale across Europe.

Microsoft — Nordic region facilities export waste heat into local district networks. Microsoft’s data centers in the Stockholm and Helsinki regions have active agreements with municipal utilities, with publicly disclosed capacity serving tens of thousands of households.

Equinix — operates waste heat recovery at its HE6/HE7 campus in Helsinki in partnership with Helen Ltd. The deployment is among the largest documented data center-to-district heating integrations in Europe by capacity.

Digital Realty — has waste heat recovery operational at facilities in the Netherlands, with Vattenfall Warmte as the utility partner. The Amsterdam deployment serves as a reference architecture for new hyperscale builds in the Rhine-Main corridor.

Eco Datacenter (Sweden) — the most comprehensive implementation, where the facility is designed from the ground up as a combined compute and district heating asset. 100% of waste heat is contractually committed to the local municipal network.

Fortum (utility side) — has published a roadmap to source 40% of Helsinki metropolitan district heating from data center waste heat by 2030, up from approximately 15% in 2025. This utility-side commitment is creating HPA pricing certainty that accelerates operator investment.

Greenfield vs Retrofit: The District Heating Integration Decision

The decision framework for district heating integration follows a different logic than HVDC or cooling architecture decisions, because proximity to existing infrastructure — not just internal design choices — determines viability.

Greenfield (New Build) — Site Selection Is the Critical Variable

For new AI campuses, the district heating decision should be made at site selection, not during design. A facility sited 500m from a 4GDH main pipe faces integration costs of €0.75M–€1.5M and a 12–18-month connection timeline. The same facility sited 5km from the nearest pipe faces €7.5M–€15M in pipe extension costs and a 3–5-year timeline.

The siting rule: For any new European AI facility above 5 MW, model the nearest 4GDH network pipe distance before committing to a site. The revenue differential over a 10-year HPA can exceed €200M for a 100 MW facility — more than enough to justify paying a premium for a proximate site.

Retrofit — Three-Factor Viability Test

For existing facilities considering district heating integration:

Factor 1 — Rack density: Below 40 kW per rack, coolant exit temperatures are typically insufficient for direct 4GDH injection without heat pumping. The heat pump adds €3–6M in CAPEX and degrades the efficiency advantage. At 60 kW+ per rack, direct injection is feasible. At 100 kW+, it is strongly favored.

Factor 2 — Pipe proximity: Apply the same distance economics as greenfield — €1.5M–€3M per km of pipe extension. Calculate the payback period for connection cost against expected HPA revenue at your local market rate. Typically, viable below 3 km at Frankfurt or Amsterdam HPA prices.

Factor 3 — Facility lifetime: Connection costs and PHE installation are sunk costs amortized over the HPA term. Facilities with less than 5 years of planned operation rarely produce favorable payback periods except in highest-price Nordic markets.

For operators assessing compute workload density before making infrastructure decisions, evaluating the AI application stack matters as much as facility design. Organizations comparing enterprise AI knowledge management systems will find that application-layer efficiency choices directly influence the sustained rack density — and therefore the heat grade — their facilities produce. Similarly, operators choosing between enterprise AI search and RAG architectures are making decisions that determine whether their compute clusters run at continuous high density (favorable for heat recovery) or bursty low utilization (unfavorable).

Competing Approaches: Why Alternatives Fall Short Above 60 kW

District heating integration is not the only way to manage waste heat from high-density AI racks. Understanding why the alternatives are inferior at Blackwell densities clarifies why the market is converging on 4GDH integration for serious deployments.

| Heat Rejection Method | Max Effective Density | Water Use | Energy Recovery | Revenue Potential | 2026 Viability |

| Air-side economizers | 15–25 kW/rack | None | None | None | Obsolete for AI |

| Cooling towers (evaporative) | 30–60 kW/rack | Very high | None | None | Water-constrained |

| Adiabatic cooling | 20–40 kW/rack | Moderate | None | None | Transitional |

| Rear-door heat exchangers | 20–40 kW/rack | Low | Partial | Minimal | Sub-optimal |

| Direct liquid cooling → air rejection | 40–100 kW/rack | High (cooling towers) | None | None | Regulatory risk |

| Direct liquid cooling → 4GDH | 100–150 kW/rack | Very low | Full | €25–45/MWh | Optimal for EU |

The key differentiator at 120–150 kW Blackwell rack density is that every alternative either fails to scale (air-side economizers, adiabatic), consumes large volumes of water (cooling towers), or rejects heat to atmosphere with no economic or regulatory return. In European markets with water scarcity concerns and EED compliance obligations, 4GDH integration is not just economically optimal — it is the only approach that simultaneously addresses density, water use, and regulatory requirements.

For operators evaluating the enterprise AI tools that will run on this infrastructure, the compute density implications of different AI platform choices are covered in our analysis of Guru vs Glean and enterprise AI knowledge platforms.

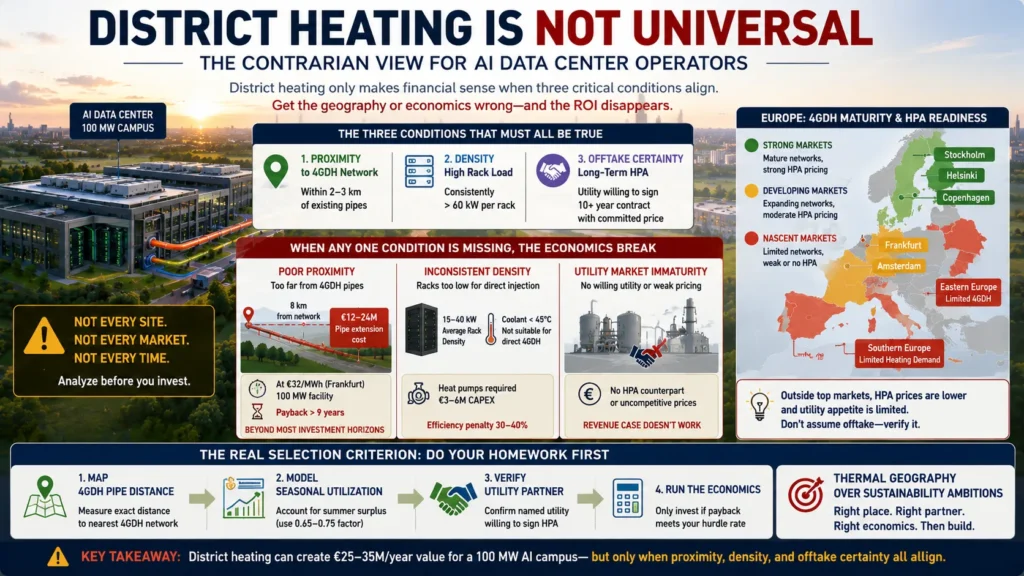

The Contrarian View: District Heating Is Not Universal

The infrastructure press has begun treating district heating integration as a universal best practice for European AI data centers. This is an overcorrection that will cost operators who apply it without the geographic and economic analysis it requires.

The financial case for district heating integration rests on three conditions that must simultaneously hold: proximity (within 2–3 km of a 4GDH network), density (rack loads consistently above 60 kW to produce injectable coolant temperatures), and offtake certainty (a utility willing to sign an HPA with committed pricing for 10+ years).

If any of these conditions is absent, the economics shift dramatically:

Poor proximity: A site 8 km from the nearest 4GDH pipe faces €12–24M in extension costs. At Frankfurt HPA prices of €32/MWh and a 100 MW facility, payback exceeds 9 years — beyond the planning horizon for most infrastructure investments.

Inconsistent density: A colocation facility running mixed workloads at 15–40 kW average rack density cannot reliably produce coolant above 45°C. Direct 4GDH injection is not viable. Heat pumps to boost temperature to usable levels cost €3–6M in CAPEX and reduce the efficiency advantage by 30–40%.

Utility market immaturity: Outside Stockholm, Copenhagen, Helsinki, Frankfurt, and Amsterdam, HPA markets are nascent. Operators in Eastern Europe, Southern Europe, or markets with limited 4GDH penetration may find no willing utility counterpart, or HPA prices too low to justify connection investment.

The real selection criterion: Before designing district heating integration into any European AI facility, map the nearest 4GDH pipe distance, model the seasonal utilization factor for your specific location, and verify that a named utility partner is willing to contract. The thermal geography of your site matters more than your sustainability ambitions.

Implementation Timeline: What to Expect

For operators who have determined that district heating integration is viable, understanding the realistic timeline prevents planning failures.

Phase 1 — Feasibility and utility negotiation (3–6 months): Thermal output modeling, pipe proximity survey, initial utility discussions, ERF projections, Article 26(6) assessment preparation. Output: HPA term sheet and connection agreement in principle.

Phase 2 — Design and permitting (4–8 months): PHE sizing, thermal substation design, Loop 2 pump specification, DLC Loop 1 integration design. Municipal planning permission for any pipe extensions required. Output: construction-ready design package.

Phase 3 — Civil works and pipe connection (4–12 months): Pipe extension construction (if required), thermal substation installation, PHE and secondary loop installation. Timeline heavily dependent on pipe extension distance and local civil permit processing speed.

Phase 4 — Commissioning and HPA activation (2–3 months): Loop integration testing, temperature stability verification, utility acceptance testing, HPA activation. First heat sales revenue begins.

Total timeline: 13–29 months from feasibility decision to first revenue — shorter for sites with existing proximate 4GDH connections, longer for sites requiring pipe extensions.

FAQ

1.What is a district heating AI data center?

Ans-A district heating AI data center is a liquid-cooled computing facility that exports its GPU waste heat to a municipal heating network rather than rejecting it to atmosphere. Blackwell-generation AI racks operating at 120–150 kW per rack produce coolant exit temperatures of 55°C–65°C — within the direct-injection range of 4th Generation District Heating (4GDH) networks. This converts what was previously a thermal liability into a monetizable energy product sold to utilities under long-term Heat Purchase Agreements at €25–45/MWh.

2.Why can AI racks produce heat that older data centers could not use for district heating?

Ans-The temperature of the waste heat determines its usability. Traditional air-cooled enterprise servers produced waste heat at 25°C–35°C — too cool for direct 4GDH injection. Bridging to the 45°C+ required by municipal networks required industrial heat pumps with significant capital and operating cost. Blackwell GPU racks with direct liquid cooling produce coolant exit temperatures of 55°C–65°C — above the 4GDH threshold without any heat boosting. The heat pump is eliminated and the economics become compelling.

3.What is ERF and why does it matter more than PUE in 2026?

Ans-ERF (Energy Reuse Factor) measures the proportion of a facility’s total energy input that is recovered and reused externally. ERF = exported reused energy ÷ total IT energy input. A facility with ERF 0.45 exports 45% of its electrical input as useful heat to the city. Under EU EED frameworks, ERF is increasingly determinative for facility permits and sovereign compute program eligibility. A facility with PUE 1.35 and ERF 0.45 may receive more favorable regulatory treatment than a PUE 1.08 facility with ERF 0.00 — because EU policy prioritizes community energy contribution, not just internal efficiency.

4.How much money can a 100 MW AI campus make from district heating?

Ans-Using Frankfurt as an example: 78 MW recoverable heat × 8,760 hours × 0.75 seasonal utilization = 512,460 MWh annually. At €32/MWh HPA price, that is approximately €16.4M in direct heat sales. Adding cooling OPEX reduction (€6.2M), carbon offset value at EU ETS prices (€6.7M), and regulatory compliance savings (€1.5–3M), total annual value reaches €30–33M. Nordic markets with HPA prices of €38–45/MWh produce proportionally higher returns.

5.What happens to the waste heat in summer when cities don’t need heating?

Ans-Summer heat surplus is a real planning challenge. District networks absorb 5–15% of rated capacity in peak summer (primarily hot water, not space heating). Mitigation strategies include: underground aquifer thermal energy storage (ATES) for seasonal buffering, secondary industrial offtake contracts with year-round heat users (food processing, pharma, greenhouses), and hydrogen production via electrolysis where local infrastructure exists. Conservative revenue models should apply a 0.65–0.75 seasonal utilization factor rather than assuming year-round HPA utilization.

6.Can existing data centers retrofit for district heating?

Ans-Yes, if three conditions hold: rack density consistently above 60 kW (lower densities cannot reliably produce injectable coolant temperatures), proximity within 2–3 km of a 4GDH network (beyond 3 km, pipe extension costs typically destroy the payback case), and planned facility lifetime exceeding 5 years. Retrofit requires PHE installation, secondary loop plumbing, thermal substation installation, and utility connection — typically €3–8M in total capital for a 50–100 MW facility, recovering within 2–4 years at current European HPA prices.

7.Which European cities have the best economics for district heating integration?

Ans-Stockholm, Copenhagen, and Helsinki offer the strongest economics: HPA prices of €35–45/MWh, the most mature 4GDH networks with highest coverage density, and utilities actively seeking data center heat supply. Frankfurt and Amsterdam are the highest-volume opportunities due to hyperscale concentration, with HPA prices of €25–36/MWh. Paris is accelerating through sovereign AI infrastructure programs. Markets to approach with caution: Eastern Europe (nascent 4GDH expansion), Southern Europe (limited heating demand seasonality), and the UK (strong economics but post-Brexit regulatory divergence from EU EED framework).

Conclusion: Waste Heat Is Now Infrastructure Value — But Only If You Plan for It

District heating AI data centers in 2026 represent the convergence of three forces that are making waste heat recovery not just desirable but essential for European AI infrastructure: the thermal physics of Blackwell liquid cooling producing directly injectable heat temperatures, the EU regulatory framework mandating waste heat assessment and penalizing non-compliance, and the financial maturity of Heat Purchase Agreement markets that can now generate €25–35M annually for a 100 MW campus.

The operators who will benefit most are not those who retrofitted existing facilities as an afterthought. They are those who treated thermal geography — proximity to 4GDH networks, seasonal demand profiles, and utility partnership availability — as a first-order site selection criterion before committing capital.

The most important decision is not which heat exchanger to specify or which utility to approach. It is whether your site is in the right place relative to the district heating network that will turn your GPU waste heat from a cooling liability into a 10-year revenue stream.

If you are planning a European AI deployment above 1 MW, model the thermal geography before you finalize the site. The hot water question may be more important than the power question.

Sources & Technical References

This article was developed using a synthesis of 2026 infrastructure data, thermal physics modeling, and European regulatory frameworks. Below are the core references used to derive the economics and engineering parameters of District Heating AI Data Centers.

- EU Energy Efficiency Directive (Recast) Article 26(6): The foundational mandate requiring data centers with a total rated energy input exceeding 1 MW to perform waste heat recovery feasibility assessments.

- Energy Reuse Factor (ERF) Framework: The specific metric used to measure the proportion of a facility’s total energy input that is recovered and reused externally, currently used for EU sovereign compute program eligibility (Target ERF ≥ 0.30).

- 4th Generation District Heating (4GDH) Technical Specifications: Engineering benchmarks for municipal networks requiring supply temperatures of 45°C–65°C, compatible with liquid-cooled Blackwell GPU exit temperatures.

- NVIDIA Blackwell Thermal Design Power (TDP) Profiles: Data regarding rack-level power density (120–150 kW) and its impact on coolant exit temperatures (55°C–65°C).

- European Heat Purchase Agreement (HPA) Index: Current 2026 market pricing ranges for waste heat sales across Stockholm, Helsinki, Copenhagen, Frankfurt, Amsterdam, and Paris.

- EU Emissions Trading System (ETS) Projections: 2026 carbon pricing (estimated at €65/tonne CO₂) used to calculate the carbon offset value of replacing natural gas heating with data center waste heat.

- Municipal Utility Roadmaps (2026–2030): Strategic plans from utility partners including Fortum Värme (Stockholm), Helen Ltd (Helsinki), and Mainova (Frankfurt) regarding data center heat integration.

- Aquifer Thermal Energy Storage (ATES) Case Studies: Technical documentation on underground seasonal buffering to manage the “Summer Heat Surplus” problem in high-density AI campuses.

Disclaimer & Transparency Note

Transparency Note: Research & Methodology This guide is the result of a multi-month analysis of the European AI infrastructure landscape as of early 2026. The data presented, including thermal output calculations, HPA pricing benchmarks, and regulatory timelines, is derived from a synthesis of municipal utility roadmaps, technical specifications for NVIDIA Blackwell-generation hardware, and the current enforcement phase of the EU Energy Efficiency Directive (EED). All financial models and ROI projections are based on mid-range European market benchmarks (e.g., Frankfurt) and incorporate a 0.65–0.75 seasonal utilization factor to account for the summer heat surplus problem.

Technical Disclaimer The information provided in this guide is for educational and strategic planning purposes only and does not constitute engineering, legal, or financial advice. Infrastructure decisions—particularly those involving high-pressure thermal loops, grid-scale power distribution, and long-term utility contracts—require site-specific validation by certified professional engineers and legal counsel.

Market Variability Warning While the economics of district heating integration are increasingly compelling for high-density AI campuses, they are highly dependent on “thermal geography”. Factors such as specific pipe proximity, local utility appetite, and national regulatory variations can significantly alter the payback periods and technical viability described herein. Readers are encouraged to conduct a site-specific Article 26(6) feasibility assessment before finalizing site selection or capital commitments.

Author Bio

Saameer is a technology journalist and infrastructure analyst covering AI systems, data center power architecture, and EU digital regulation. He focuses on the operational gap between vendor promises and real-world deployment economics, with ongoing analysis of sovereign AI infrastructure and advanced cooling systems across Europe.