By 2026, Tier-1 enterprises have quietly rewritten their outsourcing playbook. The decisive variable is no longer developer headcount or hourly rates—it is where AI workloads physically execute. As banks, hyperscalers, and regulated enterprises deploy agentic AI systems handling billions in capital exposure, the competition between Central and Eastern European (CEE) hubs has shifted from talent arbitrage to infrastructure physics. In this new reality, Warsaw is not merely competing with Bucharest on cost—it is outpacing it on compute sovereignty, GPU proximity, and latency discipline.

Key Takeaways

- GPU Proximity beats cheap talent: Local Nvidia H100 and Blackwell clusters in Warsaw reduce inference and training latency below Tier-1 risk thresholds.

- Latency is now a balance-sheet variable: 10–30ms round-trip differences translate into measurable execution risk for agentic AI systems.

- Poland’s higher flat tax (Ryczałt) functions as a trust filter, not a cost penalty.

- Romania remains a talent powerhouse, but its AI workloads still depend on cross-border compute relay.

- Warsaw’s advantage is structural, regulatory, and energy-backed, making it compounding—not cyclical—through 2026.

Information Gain

Most Poland–Romania comparisons still rely on wage charts and tax percentages. This article introduces decision primitives now used by Tier-1 procurement, risk, and compliance committees:

- GPU Proximity: Physical adjacency to high-density AI compute.

- Latency Arbitrage: The hidden cost of routing AI workloads across borders.

- Inference Lag: Performance degradation when heavy models rely on non-local GPUs.

- Compute Sovereignty: Legal necessity under EU Data Act 2026 for localized AI training.

Together, these explain why Warsaw attracts premium contracts despite higher fiscal overhead.

Deep Analysis

The 2026 AI Power Gap

Warsaw’s Wola and Praga districts have evolved into a CEE GPU cloud nucleus, anchored by hyperscaler capital and Tier-4 data center capacity. With Google Cloud Region Warsaw and Microsoft’s Polish Azure Region operating on-soil Nvidia H100 and Blackwell (GB200) clusters, enterprises achieve sub-5ms local latency for training and inference—well within thresholds required for autonomous trading, credit decisioning, and AML automation.

Romania, by contrast, remains optimized for fiber-speed transit rather than compute density. Bucharest-based teams frequently relay AI workloads to Frankfurt or other Western European Tier-4 facilities. For conventional enterprise software this is acceptable. For agentic AI—where thousands of micro-calls execute per second—it introduces a measurable Latency Tax.

Infrastructure Arbitrage Bridge:

The shift we are witnessing is a move from labor arbitrage to infrastructure arbitrage. While a senior developer in Bucharest may cost 10–15% less, the inference lag created by routing AI calls to Frankfurt can cost enterprises millions in execution inefficiency and model instability. In 2026, the cheapest developer often becomes the most expensive choice if they are physically disconnected from the GPU core.

Energy Grid Reality: The SMR Hedge

AI infrastructure is now power-constrained before it is talent-constrained. Poland’s roadmap for Small Modular Reactor (SMR)-backed data centers, supported by nuclear and renewable investment partnerships with U.S. firms such as GE Hitachi, provides a 2030 energy-security hedge for high-density AI. Romania’s hydro- and wind-heavy grid, while environmentally strong, has yet to demonstrate the same stability for sustained GPU saturation at scale.

Regulatory Inevitability: EU Data Act 2026

The EU Data Act, fully enforceable across 2025–2026, mandates that highly sensitive financial and operational data must be processed within local jurisdictional clouds. For Tier-1 banks, this converts Warsaw’s local Azure and Google regions from a performance preference into a legal requirement, eliminating cross-border AI training for regulated workloads.

Sovereignty Callout:

In 2026, “Sovereign AI” is no longer a buzzword; it is an insurance requirement. Tier-1 banks are finding that insurers are refusing to underwrite AI-driven credit and trading risks if training data leaves the local jurisdictional cloud.

Case Study / Real-World Scenario

A direct consequence of this infrastructure gravity is talent migration. Senior Romanian engineers increasingly relocate to Poland to access regulated, GPU-adjacent projects, as documented in Romanian Developers Moving to Poland in 2026

https://techplustrends.com/romanian-developers-moving-poland-2026/

Winners vs Losers

| Dimension | Poland (Warsaw) | Romania (Bucharest) |

| AI Contract Tier | Tier-1 Banks & Big Tech | Tier-2 / Hybrid |

| GPU Access | Local H100 & Blackwell | Mostly cloud-relay |

| Fiscal Model | Higher flat tax, high trust | Lower tax, higher scrutiny |

| Enterprise Perception | Audit-ready | Cost-efficient |

(Reference: https://techplustrends.com/romania-vs-poland-senior-java-architect-tax-2026/)

Comparison Matrix

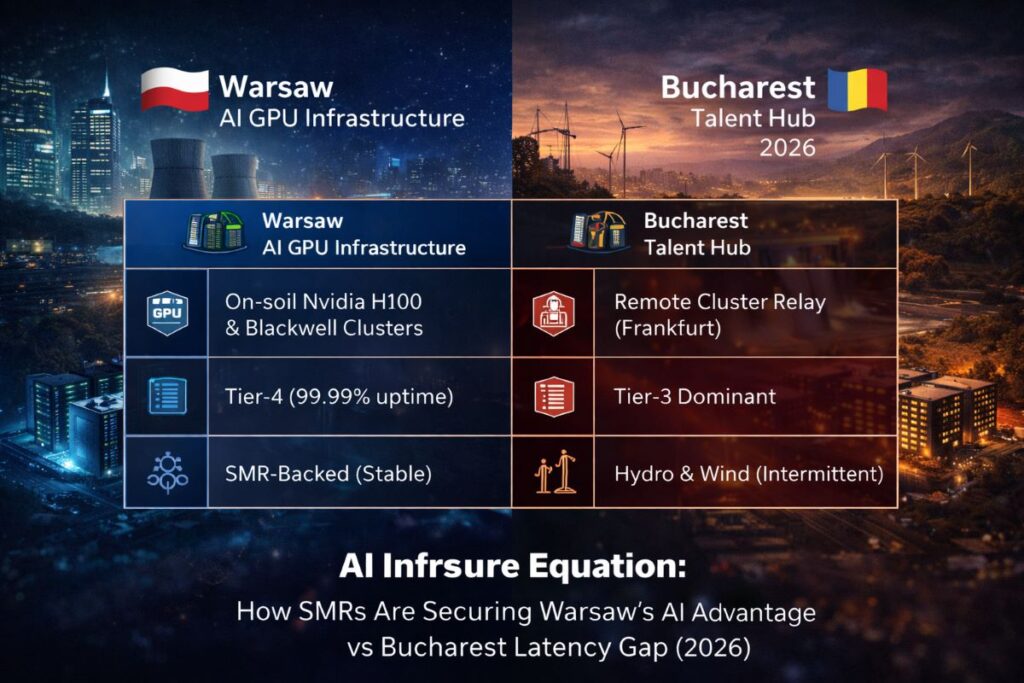

| Feature | Warsaw (AI Hub) | Bucharest (Talent Hub) |

| GPU Availability | On-soil clusters | Remote clusters |

| Data Centers | Tier-4, 99.99% uptime | Tier-3 dominant |

| Energy Grid | Nuclear + SMR roadmap | Hydro/Wind, less stable |

| Cloud Regions | Local Google & Microsoft | Regional nodes |

(Reference: https://techplustrends.com/outsourcing-poland-vs-romania-2026-costs/)

(Reference: https://techplustrends.com/warsaw-ai-infrastructure-vs-bucharest-2026/)

(Reference:https://techplustrends.com/java-25-migration-warsaw-banking-b2b-gold-mine/)

“Comparison table of Warsaw AI GPU infrastructure vs Bucharest talent hub 2026 showing latency differences and SMR energy grid readiness.”

CoE Framing (Center of Excellence Perspective)

From a Center of Excellence perspective, Warsaw offers a complete enterprise trust stack: KSeF 2.0 e-invoicing, NIS2 alignment, and predictable audit enforcement. This reduces systemic risk for AI programs handling regulated capital flows, reinforcing why enterprises accept higher operating costs.

(Reference: https://techplustrends.com/central-europe-it-contractor-tax-audit-2026/)

(Reference: https://techplustrends.com/warsaw-banking-in-region-mandate-java-25/)

Strategic Implications for 2026

- Tier-1 banks will formalize local GPU execution as a procurement requirement.

- Talent-only hubs will face rate compression.

- Warsaw will attract not just projects, but decision authority and risk ownership.

Why This Matters (Second-Order Effects)

Compute density reshapes labor markets, tax tolerance, and capital allocation. As Warsaw consolidates its role as a sovereign AI execution zone, it will command premium rates and institutional trust across Europe.

What To Do Now

- Enterprises: Audit latency exposure and data locality across AI pipelines.

- Contractors: Position for compliance-heavy, GPU-adjacent work—even at higher tax rates.

- Policy makers: Treat compute density as national economic infrastructure.

FAQs

1.Is Poland just cheaper than Romania?

Ans-No. Warsaw wins on technological and regulatory superiority.

2.Why does latency matter financially?

Agentic AI systems fail non-linearly beyond latency thresholds.

3.What is GPU Proximity?

Ans-Physical adjacency to AI compute clusters enabling real-time execution.

4.Why accept higher Ryczałt taxes?

Ans-They signal enterprise readiness and reduce compliance risk.

5.Will Romania catch up?

Ans-Yes—but only with sustained hyperscaler and grid investment.

6.Are Tier-1 banks already shifting?

Ans-Yes. Local compute is increasingly mandated, not optional.

Final Takeaway

In 2026, Warsaw’s advantage is not cheaper labor—it is physics, power, regulation, and trust. For enterprises deploying AI where milliseconds and compliance define outcomes, Warsaw has become the technologically superior destination in CEE.

Sources

- Tech Plus Trends internal infrastructure and fiscal audits (2025–2026)

- EU Data Act 2026 regulatory framework

- Hyperscaler infrastructure disclosures

Author Bio

Saameer Go is a senior technology journalist and analyst covering enterprise software, AI platforms, infrastructure, and EU technology regulation. With over 15 years of experience analyzing how policy, labor markets, and architecture decisions intersect, he focuses on long-term structural shifts rather than short-term hype.

Disclaimer & Transparency Note

1. Not Professional Advice: This article is for informational and strategic analysis purposes only. It does not constitute legal, tax, or investment advice. Infrastructure availability, tax regulations (including the 12% Ryczałt), and market rates are subject to rapid change under the EU Data Act 2026 and local legislative shifts. Readers should consult with qualified tax advisors or legal counsel before making cross-border relocation or procurement decisions.

2. AI Usage Disclosure: Portions of the data analysis and technical formatting in this article were supported by Generative AI and fact-checked by our editorial team. In accordance with the EU AI Act 2026, we maintain a “Human-in-the-loop” policy to ensure all hardware specifications and regulatory references are verified against hyperscaler disclosures and current legal drafts.

3. Accuracy & Omissions: While we strive for “Sub-5ms” accuracy in our reporting, technical infrastructure maps and energy grid projections (SMRs) are based on currently available 2026 roadmaps. Tech Plus Trends is not liable for discrepancies in external hyperscaler performance or legislative amendments.