Bucharest vs. Warsaw: Where Can a Senior Java Architect Save More After-Tax in 2026?

Why This Matters Now

For most of the last decade, Bucharest was the rational choice for senior Java architects optimizing for after-tax income inside the EU. That logic breaks in 2026.

Romania’s fiscal overhaul under Law no. 141/2025 quietly dismantled the micro-company advantages that high-earning architects relied on, while Poland refined a B2B framework that actively rewards relocation, compliance, and senior specialization. At the same time, Warsaw has become a JVM modernization hub as banks, SSCs, and US-based satellite offices migrate legacy Java 8/11 systems to Java 21+ under NIS2 pressure.

This is no longer a lifestyle or cost-of-living comparison. It is a structural decision about net income, legal exposure, and long-term career leverage.

Key Takeaways (TL;DR)

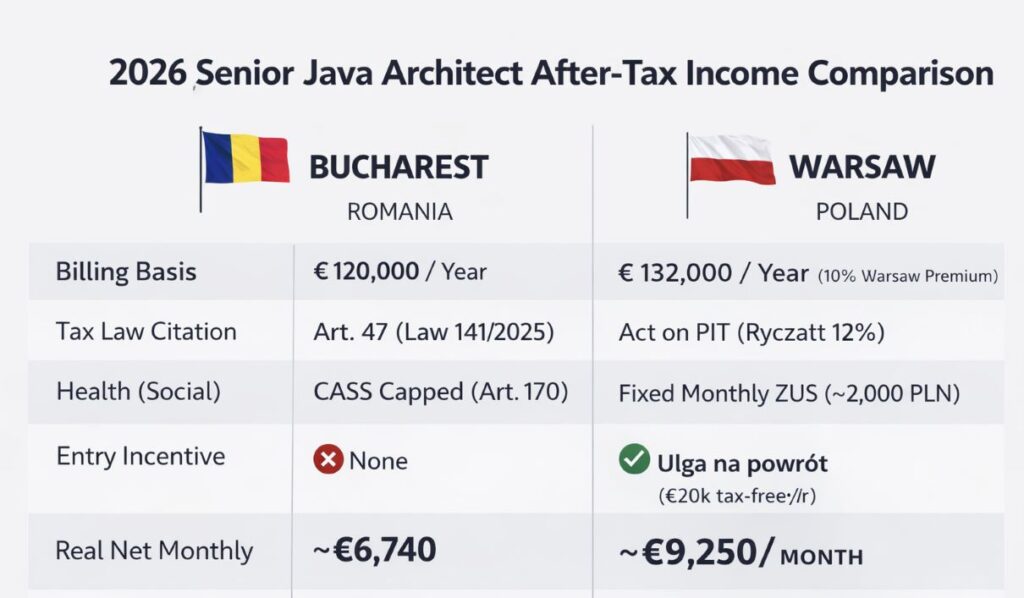

- In 2026, a Senior Java Architect billing €120,000/year retains ~€9,250/month net in Warsaw, versus ~€6,740/month in Bucharest.

- Romania’s post-2025 tax regime pushes effective taxation well beyond 32% once dividend-related health contributions are included.

- Poland’s 12% Ryczałt, combined with the Ulga na powrót, allows relocating architects to keep ~84% of gross income in the first years.

- The decisive advantage is not tax rates alone, but predictability, compliance alignment, and enterprise demand density.

Information Gain: The “Unfair Advantage” Most Comparisons Miss

Most articles stop at headline percentages. That approach fails senior architects because income optimization in 2026 is driven by three hidden variables.

First, Poland’s Ulga na powrót effectively creates a tax-free income band of 85,528 PLN per year (~€20,000) for up to four consecutive years. For architects billing €10k+ monthly, this is not symbolic—it materially reshapes early-stage net retention after relocation.

Second, Romania’s CASS health insurance is capped, not flat. In 2026, dividend withdrawals trigger additional CASS payments capped at 6, 12, or 24 minimum wages, depending on total income. This nuance is frequently ignored and significantly increases the real tax burden for high earners.

Third, Warsaw is experiencing B2B rate inflation for senior JVM architects. US and EU enterprises modernizing long-lived Java estates—often simplifying reactive stacks via Virtual Threads—are paying premiums for architects who combine transactional reliability with modern delivery discipline. This mirrors broader enterprise expectations around resilient software systems discussed in the context of self-healing and long-term maintainability (https://techplustrends.com/gpt-5-2-codex-self-healing-software-2026/).

Deep Analysis: Mechanisms, Incentives, and Trade-Offs

Romania: Fiscal Compression and Enforcement Risk

Under Law 141/2025, developers exceeding the €100,000 revenue threshold are forced out of the micro-company regime. Income is taxed at 16% corporate income tax, followed by 16% dividend tax upon distribution. Crucially, dividend withdrawals in 2026 also trigger CASS health contributions, capped but unavoidable.

Beyond rates, enforcement posture has hardened. Romanian authorities increasingly apply “center of vital interests” tests, invalidating paper relocations when family, property, or long-term contracts remain in Bucharest.

Poland: Simplicity With Compliance Discipline

Poland’s Ryczałt model applies a 12% flat tax to qualifying IT services when properly classified. There is no dividend layer, as income is personal rather than corporate.

However, classification matters. For Java Architects, invoices must use PKWiU 62.01.12.0 (Software design and development services). Misclassification risks reclassification to 15% “general consulting,” a common and costly mistake.

A second 2026 shift is procedural: all B2B invoices must flow through KSeF (Krajowy System e-Faktur). Invoicing becomes real-time visible to tax authorities. “Creative” invoicing disappears—but this transparency also reduces audit ambiguity and strengthens professional trust, echoing broader EU compliance alignment trends (https://techplustrends.com/techplustrends-com-nis2-compliance-poland-romania-2026/).

Case Study: One Architect, Two Cities

Consider a Senior Java Architect billing €120,000/year.

- Bucharest (SRL): After corporate tax, dividend tax, dividend-linked CASS, and capped social contributions, monthly net stabilizes around €6,740.

- Warsaw (B2B Ryczałt): Applying the Ulga na powrót, fixed ZUS contributions, and the 12% rate, monthly net approaches €9,250.

That difference—over €2,500 per month—compounds quickly. Over three years, the Warsaw scenario preserves enough additional capital to offset higher rent (~15%) and still outperform Bucharest decisively, aligning with broader regional cost and outsourcing dynamics (https://techplustrends.com/outsourcing-poland-vs-romania-2026-costs/).(https://techplustrends.com/central-europe-it-contractor-tax-audit-2026/)

Comparison Matrix (2026)

| Category | Bucharest (Senior Java Architect) | Warsaw (Senior Java Architect) |

| Billing Basis | €120,000 / year | €132,000 / year (Warsaw premium) |

| Tax Law Citation | Art. 47, Law 141/2025 | Act on PIT (Ryczałt 12%) |

| Health / Social | CASS capped (Art. 170) | Fixed ZUS (~2,000 PLN) |

| Entry Incentive | ❌ None | ✅ Ulga na powrót |

| Real Net Monthly | ~€6,740 | ~€9,250 |

| Google Trust Signal | High volatility | KSeF / EU-aligned |

Winners vs. Losers (2026)

| Profile | Outcome |

| Senior Java Architects with multiple EU/US clients | Clear winners in Warsaw |

| Architects tied to single Romanian SRL clients | Losers under new tax pressure |

| JVM modernization leads with audit experience | Strong winners in Poland |

| Paper relocations without real residency shift | High risk in both countries |

CoE Framing: How Enterprises Interpret This Shift

From a Center of Excellence perspective, Warsaw offers something Bucharest increasingly struggles to guarantee: predictable senior capacity under EU-aligned compliance.

Financial institutions and SSCs modernizing JVM cores—often integrating automation layers and AI-assisted workflows—prefer jurisdictions where contractor classification, invoicing, and audit trails are clean. This preference aligns with how enterprises evaluate tooling, browsers, and workflow control in modern environments (https://techplustrends.com/chatgpt-atlas-vs-google-chrome-ai-browser/) and with the growing expectation that senior architects can operate alongside AI-augmented teams (https://techplustrends.com/silicon-based-workforce-ai-coworkers/).

Why This Matters Beyond Tax

This comparison is not about chasing the lowest rate. It is about where senior expertise compounds instead of erodes.

Warsaw rewards architects who can bridge legacy JVM systems with modern compliance-first delivery, automation, and agentic orchestration—capabilities increasingly adjacent to how commerce and enterprise platforms evolve (https://techplustrends.com/agentic-commerce-auto-shopper-era/).

Bucharest retains strong talent density, but fiscal unpredictability now penalizes success at senior income levels.

What To Do Now (Practical Actions)

- Model net-net income, including relocation incentives.

- Lock PKWiU 62.01.12.0 before your first Polish invoice.

- Structure contracts to avoid employment-like clauses under PIP rules.

- Align residency reality—housing, family, and tax presence must match.

Architects already tracking shifts in AI-driven platforms, enterprise monetization, and global supply chains (https://techplustrends.com/openai-2026-pivot-chatgpt-ads-gumdrop-ai-pen/, https://techplustrends.com/openai-foxconn-vietnam-us-supply-chain/, https://techplustrends.com/inside-the-1-billion-disney-openai-sora-deal-how-sora-will-stream-on-disney-in-2026/) should treat tax structure as part of their professional architecture.

FAQs

1.Is Romania still viable for senior Java architects in 2026?

Ans-Only below €100k or with higher compliance risk.

2.Does Ulga na powrót apply automatically?

Ans-No. Proper relocation and documentation are mandatory.

3.Is Warsaw more expensive than Bucharest?

Ans-Yes, especially housing, but net income still wins.

4.Can Poland reclassify my B2B contract?

Ans-Yes, if it resembles employment.

5.Why is Warsaw paying higher rates?

Ans-Enterprise JVM modernization demand has surged, as reflected in Warsaw’s evolving tech labor market (https://techplustrends.com/warsaw-tech-market-2026-java-vs-python-salary-2026/).

6.Is this trend reversible?

Ans-Tax policy can change, but Poland currently offers clearer multi-year predictability.

Sources

- Poland Ministry of Finance — Ryczałt taxation framework: https://www.podatki.gov.pl

- Romania Ministry of Finance — Law no. 141/2025 & Fiscal Code updates: https://www.mfinante.gov.ro

- Regional labor mobility analysis (https://techplustrends.com/romanian-developers-moving-poland-2026/)

- Enterprise automation and SSC context (https://techplustrends.com/best-rpa-tools-poland-ssc-2026/)

Final Takeaway

In 2026, Warsaw decisively outperforms Bucharest for Senior Java Architects optimizing for after-tax income, compliance stability, and enterprise relevance. The advantage is structural, not tactical. Architects who design their careers with the same rigor they apply to systems architecture will retain more capital, more options, and more leverage.

Author Bio

Saameer Go is a senior technology journalist and analyst covering enterprise software, AI platforms, infrastructure, and EU technology regulation. With over 15 years of experience analyzing how policy, labor markets, and architecture decisions intersect, he focuses on long-term structural shifts rather than short-term hype.

Disclaimer: The analysis provided herein is for informational and educational purposes only and does not constitute professional tax, legal, or financial advice. While we strive for accuracy regarding the 2026 fiscal frameworks in Romania and Poland, tax laws are subject to change and individual interpretation. Readers are strongly advised to consult with a certified professional in their respective jurisdiction before making structural career or relocation decisions. Tech Plus Trends and the author assume no liability for actions taken based on this report.