The 2026 Opportunity: Why NIS2 Is Pushing Cyber Salaries and Tax Benefits

France’s cybersecurity labor market in 2026 is being reshaped by regulation rather than innovation cycles. The enforcement phase of the NIS2 Directive, combined with France’s National Cybersecurity Strategy (2026–2030), has turned senior cybersecurity engineers into regulated-risk mitigators rather than cost centers.

For employers, non-compliance carries board-level liability. For engineers, this has translated into higher gross offers—but also sharper exposure to France’s progressive tax system. Article 155 B of the French General Tax Code (the Impatriate Tax Scheme) sits at the intersection of these forces, acting as a temporary compensation stabilizer for foreign talent.

Key Takeaways

- Article 155 B can reduce the effective income tax burden by €10k–€15k per year for eligible cybersecurity engineers in 2026.

- Eligibility hinges on the reference salary test, not job title or “rarity” claims.

- Engineers must choose carefully between Option A (50% global cap) and Option B (20% foreign workday cap) to maximize net outcomes.

- The 30% exemption applies to income tax only; CSG/CRDS (~9.7%) still applies to exempt income.

- The benefit is strictly time-limited (8 years), creating a predictable “Year 9” compensation cliff that requires advance planning.

Decoding Article 155 B: The 30% Bonus and 50% Passive Income Rule

Article 155 B provides income tax exemptions, not social charge exemptions. Understanding the mechanics matters more than the headline percentage.

The 30% “Flat-Rate” Option vs. Defined Bonus

Engineers may benefit from:

- A contractually defined impatriation bonus, or

- A flat-rate 30% exemption applied to qualifying remuneration.

Both require that post-exemption taxable salary remains aligned with a French reference salary.

Cross-Border SOC Roles: The 20% Foreign Workday Exemption

Salary attributable to workdays performed outside France may be exempt, subject to two capping mechanisms under Article 155 B. Option A: total exemption capped at 50% of pay; Option B: foreign workdays capped at 20% with the bonus uncapped.

Managing US-Sourced RSUs and Dividends: The 50% Discount

Certain foreign-source dividends, interest, and capital gains may receive a 50% income tax exemption. For engineers with US RSUs or equity portfolios, this can rival the salary exemption—subject to sourcing rules.

Compliance Guardrails: Avoiding the “Reference Salary” Trap

How the French Tax Office (DGFiP) Benchmarks Cyber Roles

The reference salary is not abstract. DGFiP benchmarks against:

- The lowest salary paid for an equivalent role

- Within the same company or comparable firms

- Over the previous three years

For a Senior Security Engineer in the Paris region (2026), this benchmark typically falls between €72,000 and €78,000. Your taxable base after exemption must exceed this range. European compensation comparisons can be referenced via Cybersecurity Net Salary Europe 2026.

The 5-Year Non-Residency Audit: What Documents to Save

Engineers must prove non-residency for the prior five calendar years. Partial years count. Utility bills, leases, and foreign tax returns are routinely requested.

Option A vs. Option B: Which Capping Mechanism Maximizes Your Net?

- Option A (Global Cap): Impatriation bonus + foreign workdays capped at 50% of total remuneration.

- Option B (Alternative Cap): Foreign workdays capped at 20% of taxable pay; impatriation bonus uncapped (reference salary must be respected).

Strategic insight: Cyber engineers who travel infrequently but negotiate large bonuses usually benefit more from Option B.

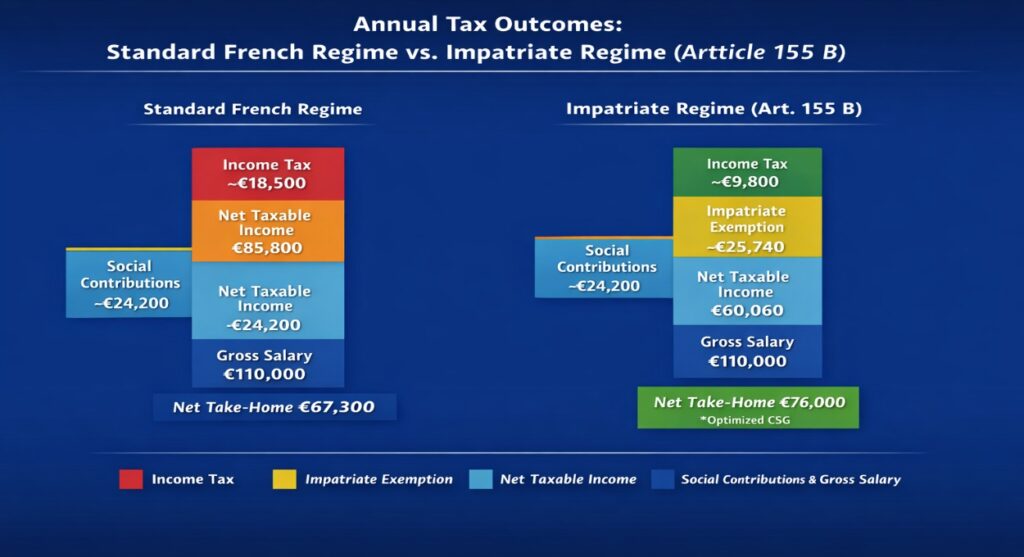

Strategic Comparison: Senior Security Engineer (€110k Case Study)

This scenario assumes a Senior Engineer recruited from London to Paris with a €110,000 gross base plus RSUs.

| Component | Standard French Regime | Impatriate Regime (Art. 155 B) |

| Gross Annual Salary | €110,000 | €110,000 |

| Social Contributions (~22%) | -€24,200 | -€24,200 |

| Net Taxable (Pre-Exemption) | €85,800 | €85,800 |

| Impatriate Exemption (30%) | €0 | -€25,740 |

| 6.8% Deductible CSG Effect | Included | Optimized |

| Net Taxable Income (Final) | €85,800 | €60,060* |

| Estimated Income Tax | ~€18,500 | ~€9,800 |

| Net Annual Take-Home | €67,300 | €76,000 |

*Note: If the reference salary for this role is €72k, the taxable base would be adjusted to €72k, slightly reducing the bonus benefit.

Analysis: By applying Article 155 B, the engineer gains ~€725 per month net, assuming post-exemption salary exceeds the reference benchmark. RSUs partially benefit from the 50% passive income exemption. This scenario highlights the critical importance of pre-signature contract clauses and starts-date alignment.

The Comparison Matrix below supplements this narrative.

Comparison Matrix: Standard French Tax vs. Impatriate Shield

| Feature | Standard Regime | Impatriate Regime |

| Gross salary | €110,000 | €110,000 |

| Income tax exposure | Progressive (up to 45%) | ~14–22% effective |

| CSG/CRDS | ~9.7% | Still applies |

| Net annual outcome | ~€72,000 | ~€84,000 (illustrative) |

The “Year 9” Cliff: Planning Your Exit Strategy

The benefit expires on December 31 of the eighth year following arrival. Engineers who fail to plan for year nine often experience abrupt net income compression without a role change. European hub comparisons are visible in CISO Berlin vs Amsterdam Net Wealth 2026.

Winners vs. Losers: The 2026 Reality Check

| WINNER | LOSER |

| External Recruits: Hired while living abroad for the last 5 years. | Local “Job Hoppers”: Engineers already resident in France who change firms. |

| Global “Field” CISOs: Those who travel 20%+ for work (extra exemptions). | Contractors: Self-employed/Freelance “Auto-entrepreneurs” do not qualify. |

| RSU-Heavy Profiles: Those with significant US tech equity. | Pure Salary Earners: Still benefit, but miss the 50% passive income shield. |

CoE Framing: Why Employers Systematically Use Article 155 B

For employers, Article 155 B functions as a Center-of-Excellence hiring instrument, not a perk:

- Attracts senior cybersecurity talent without inflating gross payroll

- Aligns compensation with EU-wide regulatory risk exposure

- Offsets rising compliance costs driven by NIS2, DORA, and sector oversight

The regime shifts cost from fixed compensation to time-bound fiscal leverage, while audit and compliance risk often sits with the employee.

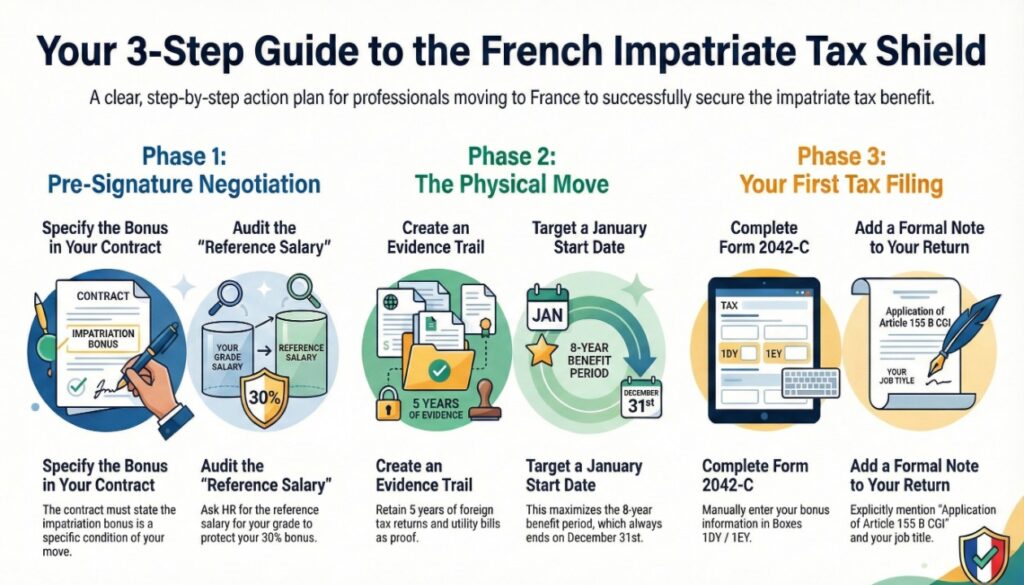

Executive Action Plan: Securing the Shield

Phase 1: Pre-Signature Negotiation

- Contractual Wording: The contract must state the impatriation bonus is a specific condition of your move.

- Reference Salary Audit: Ask HR for the “Reference Salary” for your specific grade to ensure your 30% bonus won’t be “eaten” by the floor.

Phase 2: The Physical Move

- Evidence Trail: Retain 5 years of foreign tax returns and utility bills.

- January Start: Align your start date with the beginning of the year to maximize the “8-year clock” (which always ends on a Dec 31st).

Phase 3: The First Filing (May 2027)

- Form 2042-C: Manually fill in Boxes 1DY / 1EY.

- Mention Expresse: Include a formal note in your return: “Application of Article 155 B CGI as a cybersecurity engineer recruited from abroad.”

Download the Article 155 B Impatriate Negotiation Checklist

Why This Matters (Second-Order Effects)

Article 155 B changes behavior and market dynamics:

- Retention distortion: Engineers may delay optimal career moves.

- Risk transfer: Employers optimize payroll while audit liability remains on individuals.

- Wealth planning compression: The 8-year limit creates predictable financial inflection points.

The regime serves as a temporary competitiveness bridge, returning to structural tax reality once it expires.

Executive FAQ: The 2026 Cyber-Tax Playbook

1. Does the “Minimum 20% Tax” (CDHR) apply to me?

Ans- No. The 2026 Finance Act explicitly excludes income exempted under Article 155 B from the 20% minimum tax calculation. However, for elite earners (>€250k), the CEHR surtax (3-4%) still applies to your full gross income, as the exemption does not reduce the CEHR base.

2. Option A vs. Option B: Which cap should I choose?

Ans-

Option A (Global 50% Cap): Best if you have a massive bonus but don’t travel. Your total exemption (Bonus + Workdays abroad) is capped at 50% of pay.

Option B (20% Foreign Workday Cap): Best if you travel for audits/SOC support. The “Bonus” part is uncapped (subject only to the reference salary), while “Workdays Abroad” are capped at 20% of taxable pay.

3. What happens if I support a US parent company?

Ans- If you spend 30 days a year working at a US headquarters, that pro-rata salary is 100% exempt from French income tax (within the caps above). This is the “multiplier” effect for global cybersecurity leads.

Strategic Implications for 2026

Across Europe, cyber compensation is increasingly shaped by regulatory exposure rather than technical output alone. Germany’s NIS2-driven personal liability stipends are now a negotiable component, detailed in CISO NIS2 Negotiation Germany 2026. France’s impatriate regime temporarily offsets this pressure—but only for engineers who structure their move correctly.

Final Takeaway

Article 155 B is a time-boxed strategic instrument. For a Cybersecurity Engineer moving to France in 2026, it offers a window to build significant wealth while tackling Europe’s most critical security challenges.

Sources & Regulatory References

- European Union — NIS2 Directive: https://eur-lex.europa.eu/eli/dir/2022/2555/oj

- ENISA — Cybersecurity Workforce Reports: https://www.enisa.europa.eu/topics/cybersecurity-skills

- German BSI Act / Cyber Liability Framework: https://www.bsi.bund.de/

- Polish Ministry of Finance / KSeF 2.0: https://www.gov.pl/web/finanse

- Warsaw Tech Market 2026 Java vs Python Salary: https://techplustrends.com/warsaw-tech-market-2026-java-vs-python-salary-2026/

Author Bio

Saameer is a senior technology journalist and analyst covering enterprise software, AI platforms, infrastructure, and EU technology regulation. With over 15 years of experience analyzing how policy, labor markets, and architecture decisions intersect, he focuses on long-term structural shifts rather than short-term hype.

1. Professional Disclaimer (The “Legal Shield”)

Disclaimer: This guide is provided for informational purposes only and does not constitute legal, tax, or financial advice. The application of Article 155 B of the French General Tax Code (CGI) is subject to strict eligibility criteria and individual circumstances. While every effort has been made to ensure the accuracy of the 2026 regulatory context (including the NIS2 Directive and CEHR/CDHR interactions), tax laws are subject to frequent legislative updates and administrative interpretation. Readers are strongly advised to consult with a qualified French tax attorney (Avocat fiscaliste) or a certified public accountant (Expert-comptable) before signing any employment contract or filing a tax return. The author and publisher disclaim any liability for actions taken based on the contents of this guide.

2. Transparency & Methodology Note

Transparency Note: 2026 Fiscal Modeling

- Data Sourcing: The salary benchmarks (€72k–€78k) and tax calculations provided in the “Cyber Shield” case studies are based on 2026 market data for the Ile-de-France region and the 2026 French Finance Act.

- Algorithm & Assumptions: Net take-home estimates assume a “Single” tax status (1 part) and do not account for specific family-based deductions (Quotient familial). Social charge deductions (including the 6.8% CSG) are calculated based on the standard 2026 rates for private-sector executives (Cadres).

- Regulatory Scope: The interactions between the NIS2 Directive and compensation levels are modeled on the projected demand for “Regulated-Risk Mitigators” in the French tech sector through 2030.

- Conflict of Interest: This research is independent. No compensation was received from the French Ministry of Finance or any recruitment firm for the production of this guide.