A 2026 Audit of Net Income, Compliance Risk, and Career Stability

Why This Matters Now

By 2026, Central Europe’s IT contracting landscape has reached an inflection point. What used to be a simple comparison of tax percentages has become a structural decision shaped by real-time invoicing, cross-border data sharing, and enterprise compliance expectations.

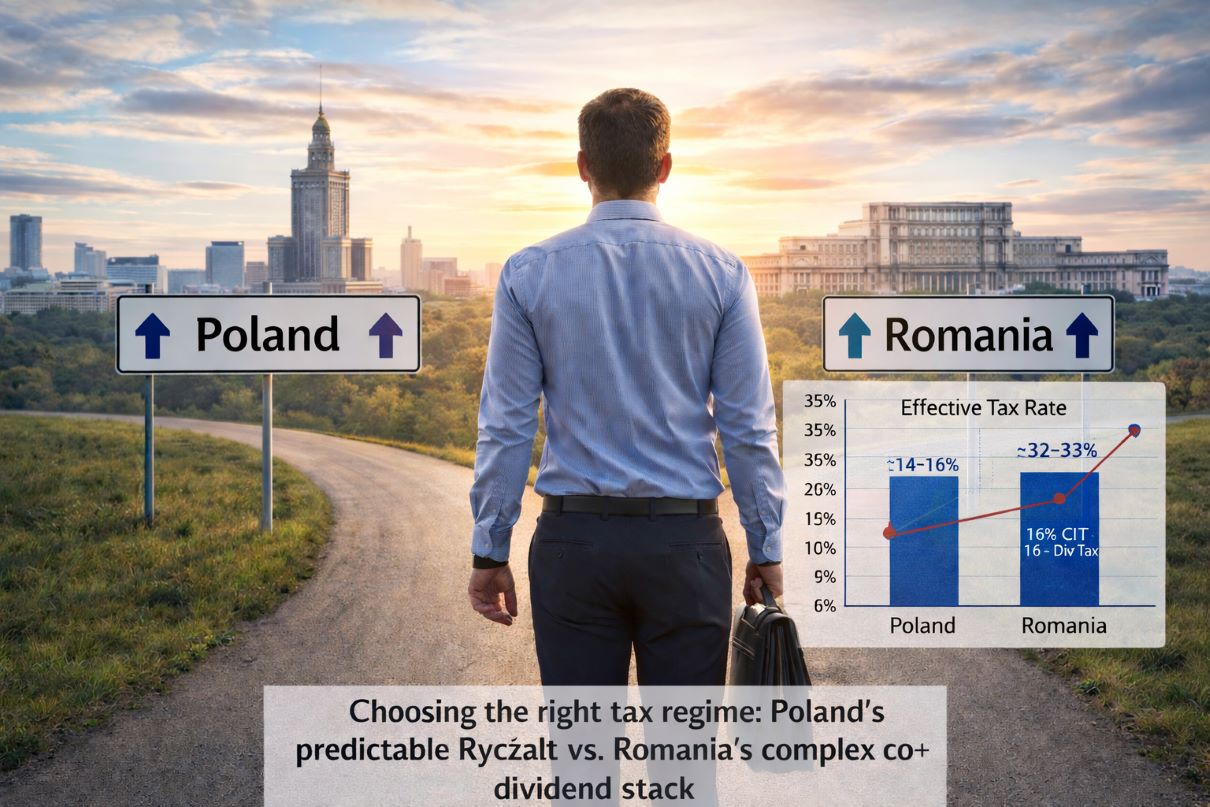

Poland, Romania, and the Czech Republic now represent three fundamentally different fiscal architectures. For contractors billing above €100,000 per year, choosing the wrong model is no longer a minor inefficiency—it can mean losing €25,000–€35,000 annually, or worse, failing enterprise audits that increasingly govern access to long-term contracts.

This article examines what actually happens after tax, after compliance, and after scrutiny.

Key Takeaways (TL;DR / SGE Box)

- Poland’s 12% Ryczałt remains the most net-efficient and enterprise-safe model for high-earning IT contractors in 2026.

- Romania’s Law 141/2025 has ended the micro-company advantage through stacked corporate, dividend, and health contributions.

- The Czech flat tax (Paušální daň) offers predictability, but caps upside for senior earners.

- KSeF real-time invoicing has become a professional trust signal, not just a compliance burden.

- In 2026, tax structure directly affects contract quality and career trajectory.

Information Gain: What Others Still Get Wrong

Most articles stop at headline tax rates. That misses the real determinant of outcomes in 2026: system design.

The decisive factors are:

- Whether social contributions are capped or cumulative

- Whether invoices are auditable in real time

- Whether the regime aligns with enterprise risk frameworks

This shift mirrors broader regulatory pressure under frameworks like NIS2, which increasingly influence how enterprises evaluate contractors across Poland and Romania

(see: https://techplustrends.com/techplustrends-com-nis2-compliance-poland-romania-2026/).

Deep Analysis: How the 2026 Systems Actually Behave

Poland — Lump Sum (Ryczałt)

Poland’s Ryczałt remains structurally simple:

- 12% flat tax for IT services

- Fixed, predictable ZUS social contributions

- Mandatory KSeF real-time invoicing

For senior contractors—especially Java architects—this transparency has become an asset. Enterprises modernizing JVM cores increasingly prefer contractors whose billing is fully KSeF-compliant, reducing procurement and audit risk. This is especially visible in Poland’s SSC-heavy automation environments

(https://techplustrends.com/best-rpa-tools-poland-ssc-2026/).

Critical detail: To retain the 12% rate, senior engineers should invoice under PKWiU 62.01.12.0 (software design and development services). Misclassification as “consulting” can trigger a 15% rate.

Romania — Corporate + Dividend Model (Post-141/2025)

Romania’s model changed fundamentally:

- 16% corporate income tax

- 16% dividend tax

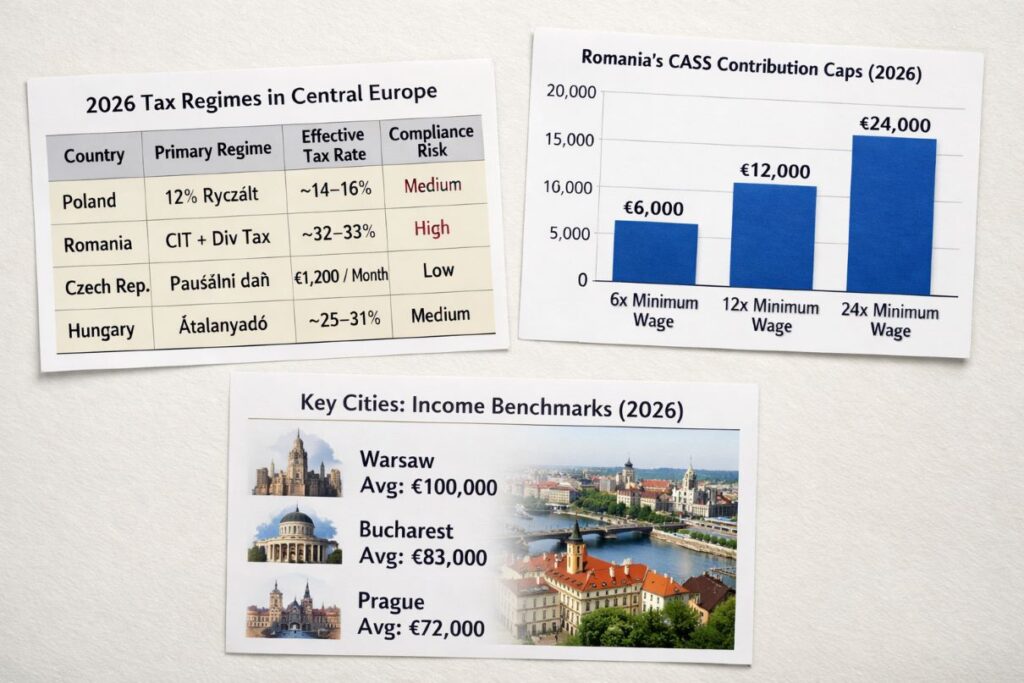

- CASS health contribution on dividends, capped at 6, 12, or 24 minimum wages depending on annual income

For high earners, this stacking pushes the effective burden above 32%, even before considering compliance uncertainty. The regime’s volatility is the primary driver behind recent contractor exits.

Czech Republic — Paušální daň (Flat Tax)

The Czech model offers:

- Fixed monthly payments by income zone

- Minimal reporting

- Low audit stress

However, for senior contractors, the trade-off is clear: predictability over maximum net income.

Comparison Matrix: Central Europe (2026)

| Country | Primary Regime | Effective Rate (High Earner) | Compliance Signal |

| Poland | 12% Ryczałt | ~14–16% (incl. ZUS) | Medium (PIP + KSeF) |

| Romania | 16% CIT + 16% Div | ~32–33% | High (Law 141/2025) |

| Czech Rep. | Paušální daň | Fixed ~€1,200/month | Low |

| Hungary | Átalányadó | ~25–31% | Medium |

Case Study: Two Contractors, One Year

A senior contractor billing €120,000 annually:

- Poland (Ryczałt): net retention near €100,000

- Romania (SRL): net retention in the low €80,000s

This gap explains the accelerating relocation trend documented among Romanian developers moving to Poland in 2026

(https://techplustrends.com/romanian-developers-moving-poland-2026/).

Winners vs. Losers (2026)

| Profile | Outcome | Reason |

| Poland-based B2B Contractors | ✅ Winner | High net + audit-friendly |

| Romanian SRL Owners >€100k | ❌ Loser | Stacked taxes + CASS |

| Czech Solo Consultants | ⚠️ Neutral | Stable but capped |

| “Paper Relocators” | ❌ Loser | Residency enforcement |

Strategic Implications for 2026

Tax strategy is now inseparable from market positioning.

- Contractors aligned with Poland’s model benefit from stronger demand and higher rate resilience, especially in Warsaw’s evolving tech market

(https://techplustrends.com/warsaw-tech-market-2026-java-vs-python-salary-2026/) - Romania’s fiscal volatility disproportionately affects senior architects comparing long-term stability

(https://techplustrends.com/romania-vs-poland-senior-java-architect-tax-2026/) - These shifts mirror broader outsourcing cost recalibrations across Central Europe

(https://techplustrends.com/outsourcing-poland-vs-romania-2026-costs/)

CoE Framing: Center of Excellence Perspective

From a Center of Excellence viewpoint, Poland’s regime offers:

- Predictable contractor ecosystems

- Lower vendor audit risk

- Seamless integration with regulated delivery pipelines

Romania’s post-141/2025 environment introduces governance friction that scales poorly in enterprise contexts.

What To Do Now

- Model three-year net outcomes, not monthly savings

- Verify correct PKWiU classification (62.01.12.0)

- Assess residency and audit exposure honestly

- Choose the system your future clients already trust

FAQs

1.Is Ryczałt still safe under KSeF?

Ans-Yes. Transparency reduces long-term audit risk.

2.What PKWiU code should senior Java architects use?

Ans-62.01.12.0 to defend the 12% rate.

3.How is Romania’s CASS calculated in 2026?

Ans-It is capped at 6, 12, or 24 minimum wages, depending on dividend income.

4.Is the Czech flat tax better than Ryczałt?

Ans-Only if predictability matters more than net income.

5.Can I relocate “on paper” only?

Ans-High risk due to EU data sharing.

6.Do enterprises care about contractor tax models?

Ans-Increasingly, yes—especially regulated clients.

Final Takeaway

In 2026, Central Europe’s tax competition is no longer about being cheapest—it is about being stable, auditable, and enterprise-aligned. Poland’s Ryczałt remains the strongest all-around architecture for high-earning IT contractors, while Romania’s reforms mark the definitive end of its tax-haven era.

Sources

- Poland Ministry of Finance — Ryczałt taxation framework: https://www.podatki.gov.pl

- Romania Ministry of Finance — Law no. 141/2025 & Fiscal Code updates: https://www.mfinante.gov.ro

- EU tax coordination directives

- Regional labor market and outsourcing data

Author Bio

Saameer Go is a senior technology journalist and analyst covering enterprise software, AI platforms, infrastructure, and EU technology regulation. With over 15 years of experience analyzing how policy, labor markets, and architecture decisions intersect, he focuses on long-term structural shifts rather than short-term hype

Disclaimer

The information provided in this article is for educational and informational purposes only and does not constitute professional tax, legal, or financial advice. While we strive to provide accurate 2026 fiscal data, including details on Romania’s Law 141/2025 and Poland’s Ryczałt framework, tax laws are subject to frequent changes and individual interpretation. Readers are strongly advised to consult with a certified tax advisor or legal professional in their respective jurisdictions before making any structural career or business decisions based on this content. Tech Plus Trends and the author assume no liability for actions taken based on the information provided herein.