The 2026 Reality Check: This Is No Longer About Saving Tax

Let’s start with an uncomfortable truth.

In 2026, choosing between 12% Ryczałt and 5% IP Box as a cybersecurity B2B contractor in Poland is no longer a simple calculation. It’s a compliance decision with real legal consequences.

I’ve spoken to CISOs, senior security consultants, and cloud security engineers who assumed IP Box was still the obvious choice—only to discover that audit risk, PIP scrutiny, and KSeF invoice matching quietly erased the savings.

Here’s the thing most calculators miss:

In 2026, the cheapest tax on paper is often the most expensive tax in real life.

This guide reframes the decision the right way—as a B2B survival strategy, not a tax hack.

The 2026 Reality Check (Kill the Myths First)

Yes, 5% still looks better than 12% on paper.

But in 2026, the hidden cost of compliance has exploded:

- IP Box eligibility was tightened to exclude most solo contractors

- KSeF exposes invoice metadata in real time

- PKWiU interpretations have hardened against cybersecurity consulting

- Solidarity Tax now meaningfully distorts high-income math

This article is not a calculator.

It is a B2B survival guide for cybersecurity professionals.

The 3 Structural Shifts That Changed Everything in 2026

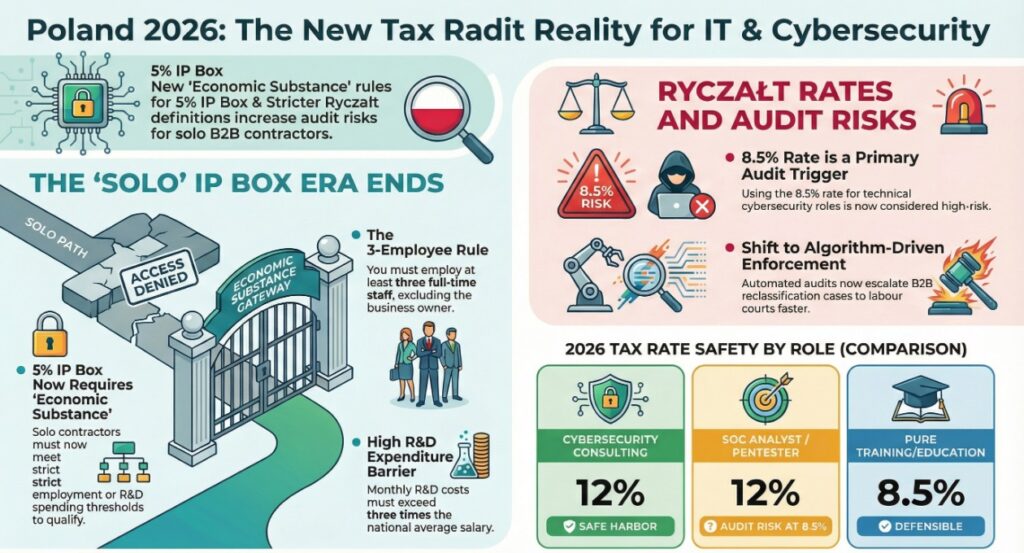

1. The 3-Employee Rule: New IP Box Eligibility Barriers

As of January 1, 2026, the Ministry of Finance effectively ended “solo IP Box” for most IT specialists.

To safely apply the 5% rate, you must now demonstrate economic substance, typically by meeting one of the following:

- Employing at least 3 full-time employees (excluding the owner), or

- Maintaining monthly R&D expenditure exceeding 3× the national average salary

For a solo pentester, SOC architect, or virtual CISO, this is usually impractical.

The market response is clear: most independent cybersecurity specialists are abandoning IP Box and defaulting to 12% Ryczałt as the compliance-safe option.

2. The PKWiU Trap: Why “Cybersecurity” Almost Always Means 12%

In 2026, tax authorities have narrowed interpretations aggressively.

- PKWiU 62.02 (IT Consulting / Cybersecurity Consulting)

→ 12% Ryczałt (safe harbor) - 8.5% Ryczałt

→ Only defensible for pure training or non-software technical support (e.g., classroom education)

Using 8.5% for roles such as:

- SOC Analyst

- Pentester

- Cloud Security Architect

…is now a primary audit trigger.

3. PIP Reclassification Risk — Updated for January 2026

This point requires precision.

In January 2026, the Prime Minister formally suspended work on granting the Labor Inspectorate (PIP) the power to reclassify B2B contracts via administrative decision.

That reform is paused.

However, the risk did not disappear — it changed shape.

While the proposal for immediate administrative reclassification was halted, enforcement pressure has shifted toward algorithm-driven audits that escalate cases into labor courts faster and with better evidence.

Translation: fewer headlines, more targeted cases.

Solo contractors on IP Box + single-client + fixed hours are still the highest-risk profile.

KSeF Compliance: Mandatory E-Invoicing Deadlines for 2026.

KSeF is not just e-invoicing. It is behavioral surveillance.

Mandatory dates:

- February 1, 2026 → Large taxpayers (>200M PLN turnover)

- April 1, 2026 → All B2B contractors

- July 31, 2026 → KSeF invoice number must appear in bank transfer titles

From mid-2026 onward:

- Invoices

- Payment flows

- Descriptions of services

…are machine-correlated across KSeF, ZUS, and tax systems.

If you claim IP Box (5%) while your invoices say “security consulting”, the system flags you automatically.

The 2026 Calculator Logic (35,000 PLN / Month Example)

Let’s ground this in reality.

Option A: Ryczałt (12%) — The “Peace of Mind” Path

- Revenue: 35,000 PLN

- ZUS: ~1,926 PLN

- Health (NFZ Tier 3): ~1,495 PLN

- Tax base after deductions: ~32,325 PLN

- Tax (12%): ~3,879 PLN

Net on hand: ~27,700 PLN

Option B: IP Box (5%) — The High-Risk Path

- Revenue: 35,000 PLN

- Costs: 2,000 PLN

- ZUS: ~1,788 PLN

- Health (4.9%): ~1,529 PLN

- Tax (5%): ~1,560 PLN

Net on hand: ~29,680 PLN

Yes—~2,000 PLN more.

But here’s what the calculator doesn’t show:

- Mandatory R&D logs

- Nexus ratio dilution risk

- Audit probability

- Retroactive tax reassessment

The Hidden Risks Most Calculators Ignore

The Nexus Trap

For solo cybersecurity specialists, purchased tools, licenses, or external consulting can dilute your Nexus ratio. A drop to 0.7 pushes your effective tax toward 15%+—worse than Ryczałt.

The PIP Reclassification Risk

Even though early-2026 proposals for immediate reclassification were paused, the Labor Inspectorate can still litigate. IP Box users are disproportionately targeted.

KSeF Invoice Matching (April 2026)

From April 2026, all B2B invoices flow through KSeF.

If your invoice says “Security Consulting” but you claim IP Box R&D income, the system may automatically trigger a compliance inquiry.

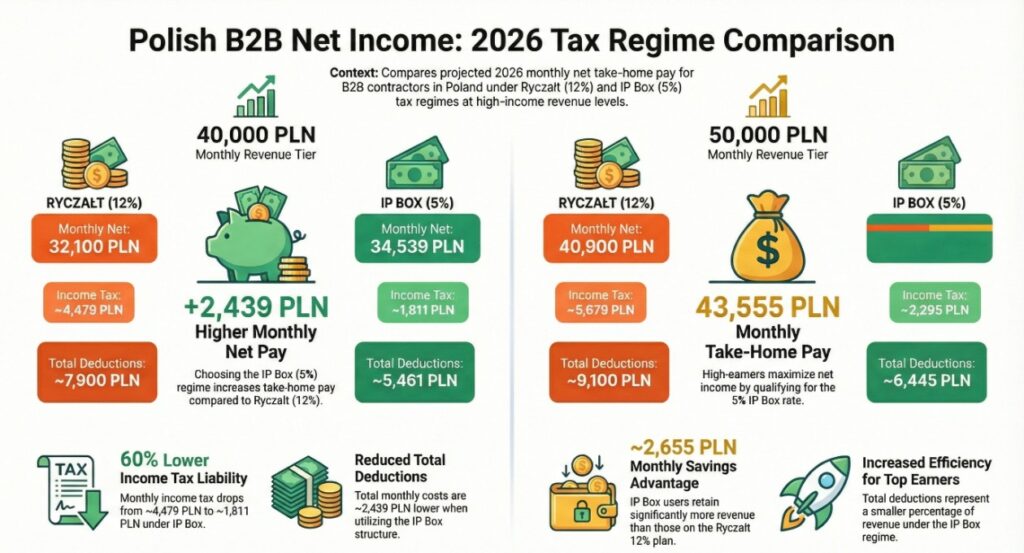

2026 B2B Net Take-Home Comparison (Monthly)

| Feature | 40k PLN (Ryczałt 12%) | 40k PLN (IP Box 5%) | 50k PLN (Ryczałt 12%) | 50k PLN (IP Box 5%) |

| Annual Revenue | 480,000 PLN | 480,000 PLN | 600,000 PLN | 600,000 PLN |

| ZUS (Social) | ~1,926 PLN | ~1,788 PLN | ~1,926 PLN | ~1,788 PLN |

| Health (NFZ) | ~1,495 PLN | ~1,862 PLN | ~1,495 PLN | ~2,362 PLN |

| Income Tax | ~4,479 PLN | ~1,811 PLN | ~5,679 PLN | ~2,295 PLN |

| Solidarity Tax | 0 PLN | 0 PLN | 0 PLN | 0 PLN |

| Total Deductions | ~7,900 PLN | ~5,461 PLN | ~9,100 PLN | ~6,445 PLN |

| Monthly Net | 32,100 PLN | 34,539 PLN | 40,900 PLN | 43,555 PLN |

Note on Solidarity Tax: In 2026, the 4% Solidarity Tax applies to income exceeding 1,000,000 PLN annually. At 50k/month (600k/year), you are still under this threshold. However, if you earn over 83,333 PLN/month, IP Box income is hit by the 4%, whereas Ryczałt remains exempt.

Why “Net Pay” Is No Longer the Right Metric

The Solidarity Tax Cliff (Danina Solidarna)

In 2026:

- IP Box income counts toward the 1,000,000 PLN threshold

- Ryczałt income does not

For a CISO earning ~1.2M PLN/year:

- IP Box triggers ~8,000 PLN in Solidarity Tax

- Ryczałt avoids it entirely

Once NFZ and compliance costs are included, Ryczałt often becomes cheaper than IP Box, despite the higher nominal rate.

This is the same logic driving senior compensation planning across Europe, as shown in broader net-pay comparisons such as the European cybersecurity net pay landscape.

The same mindset shows up in:

Net-pay comparisons across Europe (EU cybersecurity net salary analysis)

Cross-border compensation decisions (net salary comparison across Europe)Executive risk negotiations tied to regulation (how CISOs negotiate NIS2 liability stipends in Germany)

The message is consistent: compliance risk is now part of compensation strategy.

30-Second Decision Flow (2026)

- Do you employ 3+ people?

→ No → Ryczałt (12%) - Is your income >1,000,000 PLN/year?

→ Yes → Ryczałt (Solidarity Tax shield) - Can you log R&D monthly and defend Nexus ratios?

→ No → Ryczałt

IP Box in 2026 is no longer for freelancers.

It is for software security firms.

The Audit-Ready Evidence Checklist (2026)

If you still pursue IP Box, you must be audit-ready monthly, not annually.

R&D Proof

- Timestamped project logs

- Git history / architectural diagrams

- Nexus cost documentation

Anti-Reclassification Shield

- Substitution clause

- Multi-client evidence

- Own equipment & tooling

- Professional liability insurance

Eligibility Proof

- ZUS filings for 3+ employees or

- R&D spend exceeding ~27,000 PLN/month

2026 Cybersecurity B2B: Ultimate Tax FAQ

1. Can I still use the 5% IP Box if I am a solo B2B contractor?

Answer: Technically, yes, but it is much harder now. Starting January 1, 2026, the Ministry of Finance has tightened the “spirit of the law.” You must either employ 3 full-time staff or prove high R&D spending. Without these, you are a “high-risk” target for audits. Most solo cybersecurity specialists are switching to the 12% Ryczałt for safety.

2. Which Ryczałt rate is correct for Cybersecurity: 8.5% or 12%?

Answer: This is the most debated question of 2026.

- 12% (PKWiU 62.02): The “Safe Harbor.” Tax authorities generally rule that cybersecurity consulting, auditing, and systems implementation fall here.

- 8.5%: Only applicable if your work is strictly “Technical Support” or “Training” that does not involve software modification.

Warning: Using 8.5% for “SOC Analyst” or “Pentesting” roles is currently a major audit red flag.

3. Does the 4% Solidarity Tax (Danina Solidarna) apply to me?

Answer: Only if your total annual income exceeds 1,000,000 PLN.

- If you are on IP Box: Yes, the income counts toward the 1M PLN limit.

- If you are on Ryczałt: No. Ryczałt remains one of the few ways in 2026 to earn over 1M PLN without triggering the extra 4% tax.

4. Can the PIP (Labor Inspectorate) force me to switch to an employment contract (UoP)?

Answer: While the 2026 reform to grant PIP “immediate reclassification” powers was halted by the Prime Minister in early 2026, the risk still exists. PIP can still sue in labor court to prove your B2B is “fictitious.” To prevent this, ensure your contract has a substitution clause and you use your own equipment.

5. Can I combine Ryczałt and IP Box in the same year?

Answer: No. You must choose your taxation form (Lump Sum vs. Scale/Linear) by January 20th. Since IP Box requires Linear or Scale taxation, you cannot use it if you have already opted for Ryczałt for that tax year.

6. How does KSeF (National e-Invoicing) affect my tax choice?

Answer: As of April 1, 2026, KSeF is mandatory for all B2B contractors. The tax office now sees your invoices in real-time. If you claim the 5% IP Box rate but your KSeF invoices describe your work as “General Consulting,” the system may automatically trigger a “Compliance Letter” asking for your R&D logs.

Sources & Regulatory References

European Union — NIS2 Directive (Directive (EU) 2022/2555)

https://eur-lex.europa.eu/eli/dir/2022/2555/oj

German Federal Office for Information Security (BSI)

https://www.bsi.bund.de/EN/Home/home_node.html

German BSI Act (BSIG), §38 (as amended by NIS2UmsuCG)

https://www.bsi.bund.de/SharedDocs/Downloads/EN/BSI/Act/BSI_Act.pdf

ENISA — Cybersecurity Skills & Workforce Reports

https://www.enisa.europa.eu/topics/cybersecurity-skills

German Federal Ministry of the Interior (BMI)

https://www.bmi.bund.de/EN/topics/it-digital-policy/cyber-security/cyber-security-node.html

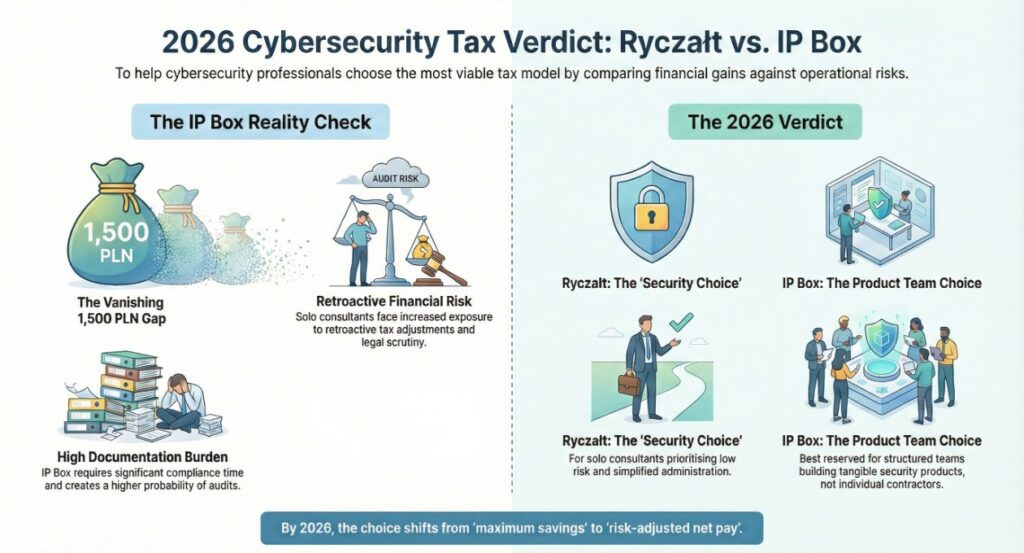

Final Verdict: 2026 Is About Risk-Adjusted Net Pay

For most cybersecurity professionals earning 35k–50k PLN/month, IP Box still looks better on paper. But once you price in:

- Compliance time

- Audit probability

- Documentation burden

- Retroactive risk

…the gap often collapses to under 1,500 PLN.

In 2026, Ryczałt is the security choice.

IP Box is for teams building real security products—not for solo consultants.

Author Bio

Saameer Go is a senior technology journalist and analyst covering cybersecurity economics, B2B taxation, enterprise risk, and EU digital regulation. With over 15 years of experience analyzing how policy, labor law, and technology architecture intersect, he focuses on long-term structural shifts rather than short-term hype.

His work specializes in the real-world impact of NIS2 enforcement, contractor reclassification risk, cross-border net pay optimization, and compliance-driven compensation models affecting CISOs and senior cybersecurity professionals across Europe. All analysis is grounded in current legislation, regulatory guidance, and practitioner-level financial modeling, not generic calculators.

Legal & Regulatory Disclaimer

Notice: The information provided in this article is for general informational and educational purposes only. It does not, and is not intended to, constitute legal, financial, or tax advice.

As of February 5, 2026, the Polish tax landscape, including the NIS2 Implementation Act, the Polish Deal (Polski Ład) updates, and IP Box regulations, is subject to frequent change and subjective interpretation by the National Revenue Administration (KAS). Every individual B2B situation is unique, especially regarding Nexus ratios and PKWiU coding. Readers should not act upon this information without seeking professional counsel from a qualified Doradca Podatkowy (Tax Advisor) or a licensed accountant specializing in the IT sector. Use of any checklists or calculators provided is at the user’s own risk.

AI Transparency Note (2026 Compliance)

Transparency Disclosure: This content was developed through a collaborative partnership between a human expert and Artificial Intelligence .

In alignment with Article 50 of the EU AI Act regarding transparency for AI-generated and AI-assisted content:

- Human Oversight: All 2026 legal dates (e.g., the April 1st KSeF deadline), Polish tax rates, ZUS thresholds, and legislative updates regarding PIP reclassification were reviewed and verified for factual accuracy by the human author (Saameer Go).

- AI Assistance: Generative AI was utilized to synthesize complex regulatory frameworks, optimize for SEO scannability, and structure comparative financial matrices.

- Editorial Responsibility: The human author maintains full editorial responsibility for the final opinions, strategic advice, and professional conclusions presented in this guide.